We believe the Fed will increase rates once before the end of the year.

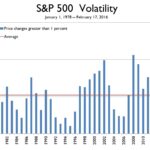

After several months of minimal volatility, September returned to form. Angst over actions from central banks across the globe coupled with the onset of corporate earnings resulted in the return to daily volatility. While we haven’t finished the month, September is looking to be one of the more volatile months of the year, as seen in the chart below.

There was a sense of complacency which reduced daily volatility; however, as we moved closer to a possible Federal Reserve rate hike, investors became a bit more uncertain.

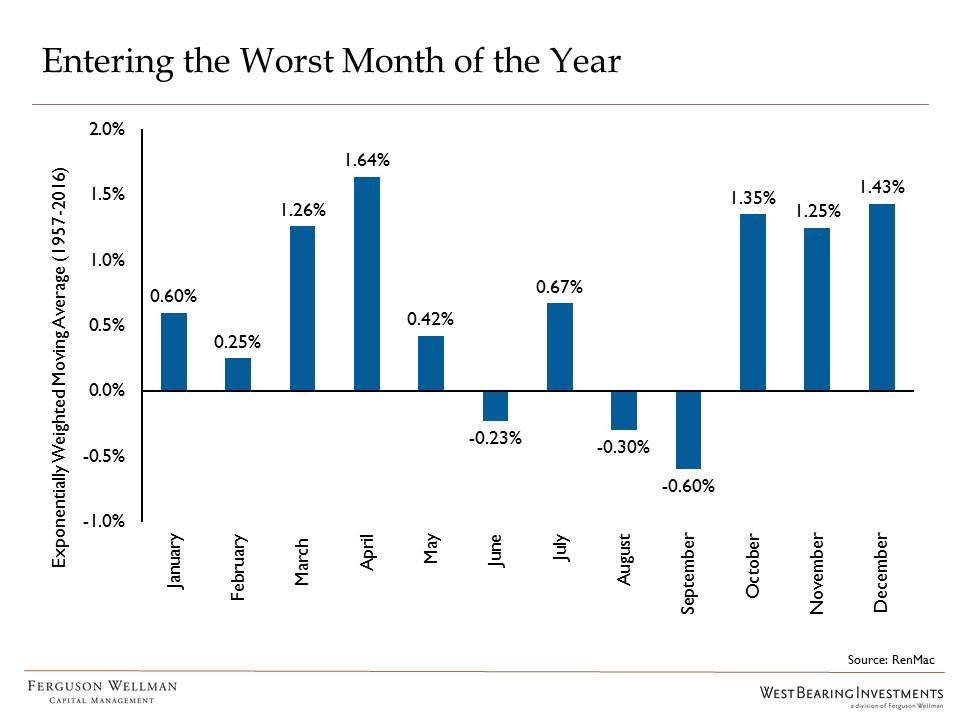

September is usually the worst month of the year for returns. As of September 22, stocks were flat for the month, which historically has been considered a win. The chart below shows that September typically delivers the worst returns and has the lowest probability of positive returns. Fortunately, looking at the calendar, the fourth quarter is a good time to be invested.

Will They Stay or Will They Go?

Earlier this month, the Federal Reserve held its benchmark rate steady at 0.25 to 0.50 percent. While Fed Chair Yellen stated that the economy has improved, she was not ready to increase rates. Despite her position, there was a shift in the board and some previous “doves” voted to raise rates. With a healthy employment market and inflation trending higher, it is going to be difficult for the Fed to maintain the current level of rates.

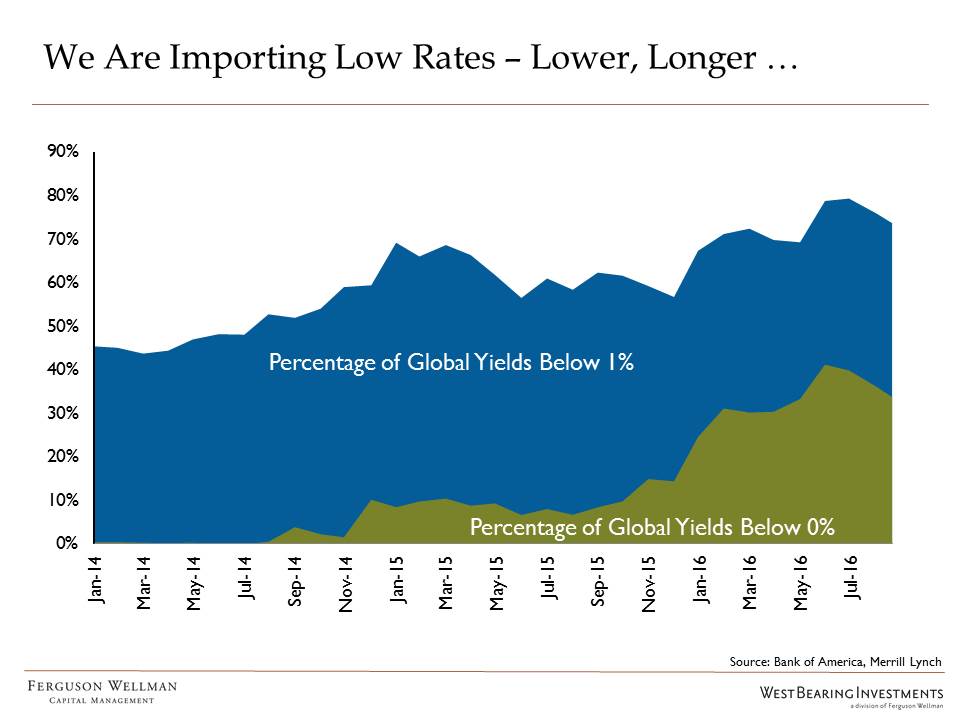

Two meetings remain for 2016, and we believe the Fed will increase rates once before year-end and that this will not result in a major shift upward in longer-term interest rates due to external factors, primarily historically low interest rates outside the U.S.

The chart below shows the amount of global sovereign debt yielding below one percent, which will put a ceiling on our longer rates moving meaningfully higher in the near future.

One place where rates have been low for a very long time is Japan. Over the last several months, the yield on the 10-year Japanese Government Bond (JGB) was under zero percent. Earlier this month, the Bank of Japan stated that they are going to target the 10-year JGB at zero percent.

This is an admission that negative yields are bad for the financial system, specifically for banking, insurance and pension funds. Time will tell if the Bank of Japan can manage this target and how it will affect the financial system. Either way, we remain cautious on Japanese equities and maintain an underweight position in client portfolios.

Jason Norris, CFA, is executive vice president of research at Ferguson Wellman Capital Management. Ferguson Wellman is a guest blogger on the financial markets for Oregon Business.