On September 17, the much anticipated Fed decision was delivered and the equity markets haven’t liked it.

On September 17, the much anticipated Fed decision was delivered and the equity markets haven’t liked it. The Fed came out and stated that while the U.S. economic growth was healthy, inflation remained below target and there was concern about global market volatility, most likely due to the Chinese market. While there was less than a 50 percent probability that they were going to hike, with the Fed commenting on external developments and sounding “dovish” at their press conference, markets are expecting more uncertainty.

Fed Chair Janet Yellen also stated that while the labor market has improved, there is still some slack. Although wages have been slow to improve, the unemployment rate continues to decline and job openings are at a record high. Because of the strength of the U.S. economy we still believe that there will be Fed hike by year-end. However, if China and the emerging markets continue to show “uncertainty,” will the Fed push off this initial raise? Unless a slowdown in China starts to have a major effect on the U.S. economy, we don’t think the Fed will wait until 2016. China, while an important market, will have shown a major slowdown before it affects the broad U.S. economy. Exports are 13 percent of the U.S. economy, and China represents 7 percent of that figure, as seen in this chart.

While some industries will have more exposure than others, we would have to see a dramatic slowdown before there would be a noticeable impact on U.S. GDP. A benefit of a slowing China is lower commodity prices and lower import prices due to a weakening currency. In essence, we are importing deflation.

Even if the Fed starts its hiking cycle, we believe it will be a lot slower than past historic cycles due to the concerns noted above. The chart below compares the 2004-2006 hiking cycle with the expectations for this immediate one, indicating that a decade ago the Fed was very aggressive in raising rates.

We believe the estimates are considerably more reasonable and thus should not have a major negative effect on the U.S. economy.

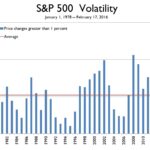

Regardless of whether then Fed hike occurs this year or next, one thing is certain … we anticipate increased volatility. The uncertainty of “when” will continue from meeting-to-meeting with the next Fed meeting occurring at the end of October. Both equities and bonds will be volatile and may present some opportunities to put some cash to work as we believe the U.S. and developed international markets will continue to improve.

- Jason Norris, CFA, is executive vice president of fixed income research at Ferguson Wellman Capital Management. Ferguson Wellman is a guest blogger on the financial markets for Oregon Business.