Uncertainty in Greece and China, along with potential interest rate hikes mean investors are looking at the market and nervously questioning where they should be invested.

We seem to have survived several weeks of hot, dry weather in the Pacific Northwest and some of those summer headlines regarding international economies may be starting to cool down as well. We have seen Greece on the verge of a “Grexit” from the Eurozone, only to get an eleventh hour bailout that was contrary to what Greek voters wanted. China released GDP growth rates and of course the numbers came right in-line with expectations at 7 percent. Corporate earnings got off to a mixed start with Apple and IBM among those hitting significant speed bumps. Lastly, Yellen made it clear that the Fed wants to start hiking interest rates in 2015. With all this news, investors are looking at the market and nervously questioning where they should be invested. We continue to believe that our clients should stay invested in equities.

While Greece filled the headlines earlier this month, the potential fallout of financial contagion was small. Several years ago, the majority of Greek debt was held primarily by European banks. Today, that liability now falls on the European Central Bank (ECB). Therefore, if there were a default, the risk of a bank failure is minimal. Whether Greece stays or “Grexits” the Eurozone, the fallout over the long term should be minimal due to the relative size of their economy. Therefore, we believe that with the ECB keeping rates low, economic growth outside of Greece should continue to improve, making Europe a compelling opportunity for equity investors.

China continues to be a wildcard. The government released above-expectation GDP growth of 7 percent for the second quarter. We’ve also seen their equity market show signs of growing pains. We have a lot of skepticism in the Chinese economic growth data as companies have been giving mixed commentary. BMW sales have dropped meaningfully. FedEx stated that their China business is showing anemic growth. Both United Technologies and IBM saw major declines in their Chinese sales. Only Apple has been an outlier, citing healthy growth and expectations to double their store footprint from 19 to 40. Our sense is that China is indeed still growing. As it moves from an industrial and infrastructure-led economy to a consumer-fueled economy, the growth rates will probably be closer to 4 or 5 percent.

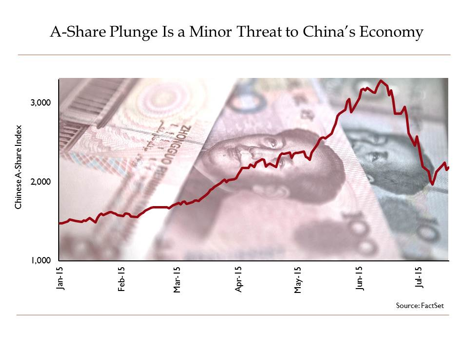

The popping of the Chinese equity A-share market has also grabbed headlines. We believe this news story is also overblown. Since the peak in June, the decline has been significant, as seen in the chart below, but the market has still realized strong growth.

A Perspective on China

- Equity investment accounts for only 12 percent of Chinese financial assets

- Only 9 percent of households participate in the equity market in China versus 49 percent here in the U.S.

- China’s growth is hindered by high debt levels, they will need growth in demand from the U.S. and Europe to reenergize their export-driven economy

- Despite a recent sell off, A-share market is still up over 100 percent in the last 12 months

- Ferguson Wellman portfolios have no direct exposure to China. We are looking for ways to gain exposure through lower risk Hong Kong market

As indicated in our recent Weekly Market Makers blog posting, we are more concerned about intervention by the Chinese government rather than the actual decline. We continue to monitor the situation and may add exposure in the Hong Kong and U.S. shares if price weakness persists. We currently have no direct exposure to mainland China.

U.S. capital markets have seen some direct effect from the headlines as well. Yellen’s testimony before Congress (Humphry Hawkins for you historians) signaled that the Fed is ready to start raising rates. Growth in the U.S. continues to trend higher, and even with the disappointing

June retail sales numbers, the numbers were not as bad as expected. We believe “lift off” will take place later this year, although the hikes will not be in a straight line. This leads us to believe that rate increases will not pinch growth in the U.S. economy; however, bond investors, particularly those in bond funds, will likely see some headwinds.

Finally, earnings season has kicked off and results have been mixed. The strong U.S. dollar has been an obstacle for revenue growth. In some instances, the translation of foreign sales-to-dollars has resulted in a 5-percent hit to earnings. In general, companies have reported in-line with estimates and the disappointments have been due to reduced guidance for future quarters. We believe this trend will continue throughout the next few weeks as companies attempt to manage the strong U.S. dollar and mixed growth outside the U.S.

While these headlines aren’t leading us to pound the table on equities, we do believe that global growth will continue to improve and valuations are in-line with long averages. Thus, we remain invested in equities with a slight tilt toward developed, international markets.

The Coin Flip

The other side of the story – from Oregon’s perspective

Summer shines favorably on the food cart industry in Oregon. Following a healthy consumption of news on international market activity, Portland professionals have a number of Greek or Chinese food cart options at their disposal.

Food Truck Empire polled dozens of food carts owners throughout the U.S. in 2014 asking what factors lead to failure. The responses certainly reflect what many of us have observed or experienced when we visit food carts that appear to be successful and stable. Supporting your favorite food carts throughout the year, not just when the weather is favorable, increases the chances that they be in a stronger position to navigate their business challenges.

Jason Norris, CFA, is executive vice president of fixed income research at Ferguson Wellman Capital Management. Ferguson Wellman is a guest blogger on the financial markets for Oregon Business.