BY JASON NORRIS | OB GUEST BLOGGER

BY JASON NORRIS | OB GUEST BLOGGER

Ferguson Wellman’s investment views on the economy and capital markets.

BY JASON NORRIS | OB GUEST BLOGGER

BY JASON NORRIS | OB GUEST BLOGGER

Each month for Oregon Business, we assess two market movers that are shaping current activity – and what they mean to investors. This posting focuses on Federal Reserve activity and recent news out of the financials sector: When the Fed will stop purchasing bonds in the open market, and whether banks will help out their troubled peers during a financial crisis.

What the Fed Said, Did or Will Do

Earlier in August, the Fed released its July meeting minutes which stated that they believe the labor markets may be healing more quickly than expected, thus leading to the possibility of increasing rates sooner-than-expected. Current expectations for the first short-term rate hike by the Fed is mid-2015. With the easing cycle nearing a conclusion, investors are left to wonder what lies ahead. When interest rates increase, bond prices decline. So when tightening begins, will we see investors start to flee bonds? And how will the equity markets respond to higher interest rates?

Our view is that short interest rates will experience most of the increase and longer-term rates will be slower to increase, thus flattening the yield curve. This will have what we call a “less negative” effect on bonds. Therefore, we are holding shorter maturity bonds, giving the ability to reinvest quicker at higher interest rates as they rise.

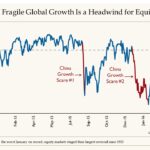

Equities, on the other hand, historically have enjoyed fairly positive performance at such times in the interest rate cycle. We were able to get some data from Cornerstone Macro highlighting previous tightening cycles (see chart below). Our takeaway from this data is that equities typically deliver positive performance over the course of the tightening. This is due to the fact that rates are moving higher due to a stronger economy, and it is not overly inflationary. While volatility usually ensues when the Fed initially acts, we believe that equity investors should “buy” that weakness.

Lending a Hand and Getting Bit

With Bank of America’s settlement of close to $17 billion earlier this month, we may see the chapter finally closing to the mortgage mess of the previous decade. JP Morgan and Citigroup have also settled with the feds. The question we have with this recent development is that most of the fines placed on these institutions were targeted not at the banks on the whole, but on divisions. For Bank of America, the fines were placed on Countrywide and Merrill Lynch. For JP Morgan, it was Bear Stearns and Washington Mutual. These companies were acquired in the depths of the financial crisis, in essence, taking on those troubled institutions “risk” so the U.S. taxpayer did not have to. This begs the question – when the next financial crisis rears its ugly head, will large, relatively healthy companies acquire troubled peers? Has the precedent been set that the U.S. government will be looking for the “fall guys?” We don’t know if JP Morgan CEO Jamie Dimon will be inclined to take on the risk of a Bear Stearns or a Washington Mutual to “help out” the U.S. taxpayer, when it may result in JP Morgan being hit with fines for the actions of those institutions pre-acquisition.

The Coin Flip

Paying homage to Oregonians Francis Pettygrove and Asa Lovejoy

We like to close our monthly blog entry by flipping our focus to living and working in Oregon. In our state and around the U.S., students are saying goodbye to summer and hello to the school year. Hopefully we all took advantage of our epic Oregon summer.

But not everyone takes advantage of summer as much as they should or could. A recent survey was released highlighting the fact that U.S. workers only take 51 percent of their eligible paid vacation. These days left on the table result in over 500 million lost vacation days a year. The survey cited “fear” as the main reason workers are less likely to utilize all of their vacation.

With the start of school, families are expected to spend more for back to school in 2014 compared to previous years. The average household will spend $670 on “back to school,” up 6 percent from last year. This is driven primarily by teenagers increasing their spending on technology.

As the saying goes, the days are long and the years are short when it comes to parenting. We suspect many students feel the same way as they say goodbye to the Oregon summer weather and head into the classrooms for another school year.

Jason Norris, CFA, is executive vice president of research at Ferguson Wellman Capital Management. Ferguson Wellman executives blog on the financial markets for Oregon Business.