There are many ways to look at economic trends. Each month, analysts at Ferguson Wellman Capital Management share how global economic data and market trends are viewed here in Oregon.

The Demise of the Consumer Has Been Overly Exaggerated

Earlier this month, several major retailers reported tough earnings. A common metric in the retail industry is Same-Store Sales (SSS), which measures the growth of the average store for a retailer. This metric standardizes industry data so it isn’t skewed by acquisitions, divestiture, etc. When three major U.S. retailers reported in May, SSS were very disappointing.

Macy’s reported a year-over-year decline of 5.6 percent. Kohl’s showed a decline of 4 percent and stalwart Nordstrom had an April decline of 1.7 percent. Our major thesis of the health of the U.S. economy is that the consumer and this headline data may give some pause to our views. However, it plays right into our beliefs about the “smarter”consumer.

Discount retailers continue to deliver accelerated growth. TJ Maxx showed SSS of 7 percent while Ross Stores grew 2.5 percent. Finally, the elephant in the room for the major retailers is Amazon.com. While Amazon doesn’t report SSS due to the fact that they don’t have any physical stores, their revenue growth over the same period grew 28 percent.

The U.S. consumer is actually spending and feeling confident. Consume confidence for May rose to its highest level in a year and retail sales, overall, are still growing right around 3 percent. So what’s changed?

Follow the Smart Money

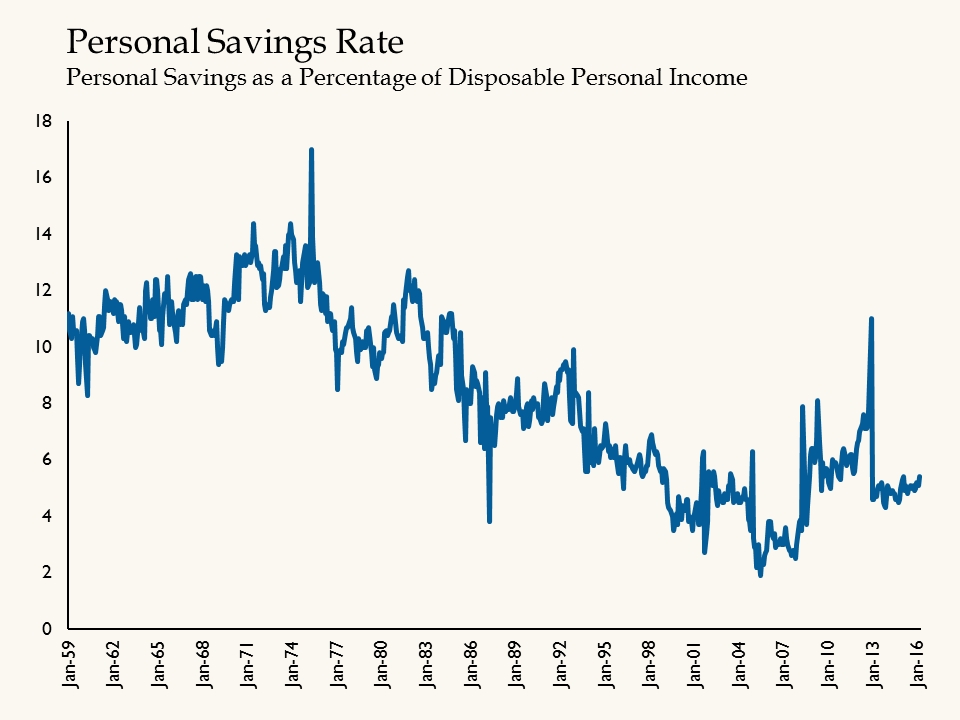

For decades, U.S. retail sales show growth of roughly 5 percent. This propelled the U.S. economy and resulted in consumer spending being over 70 percent GDP. We know that wages haven’t shown growth of over 5 percent, so how did this occur? It was savings depletion. The chart below shows the savings in the United States over the last 40 years. While not a perfect number, it is indicative of the two major trends that we have seen.

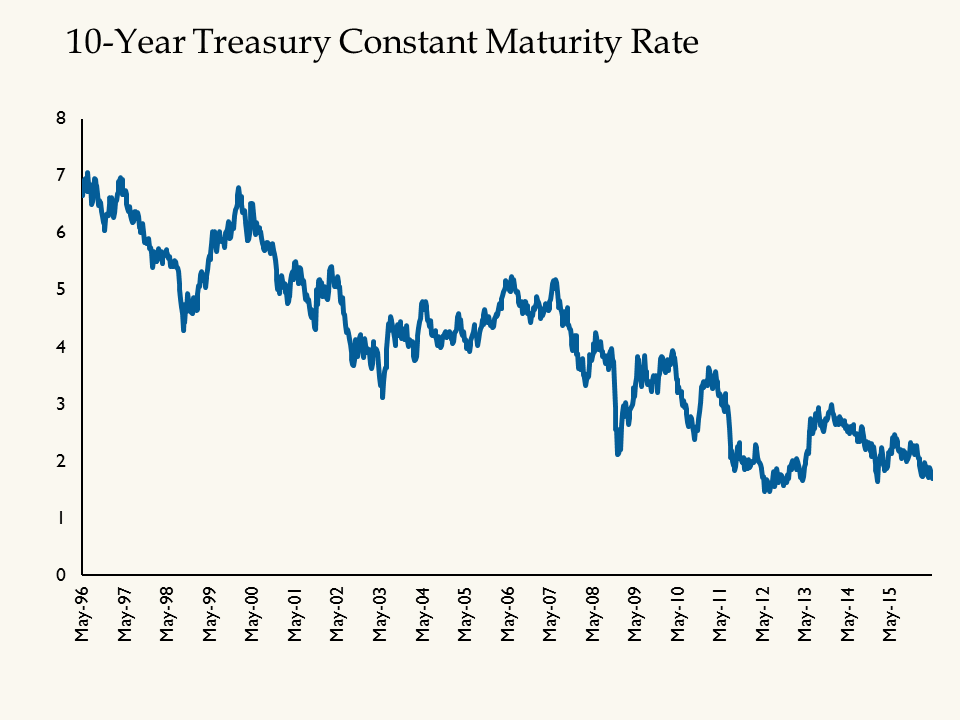

Since the recession of the early 1980s, the savings rate has shown a steady decline through the mid-2000s. Thirty years ago, consumers saved over 10 percent of their paycheck and in the early part of this decade, savings rates got as low as 3 percent. This resulted in the pace of U.S. spending to increase faster than wage growth. However, this wasn’t the only catalyst. Beyond reducing savings, consumers took on more debt. This was driven by a major decline in interest rates (see chart).

Source: Federal Reserve

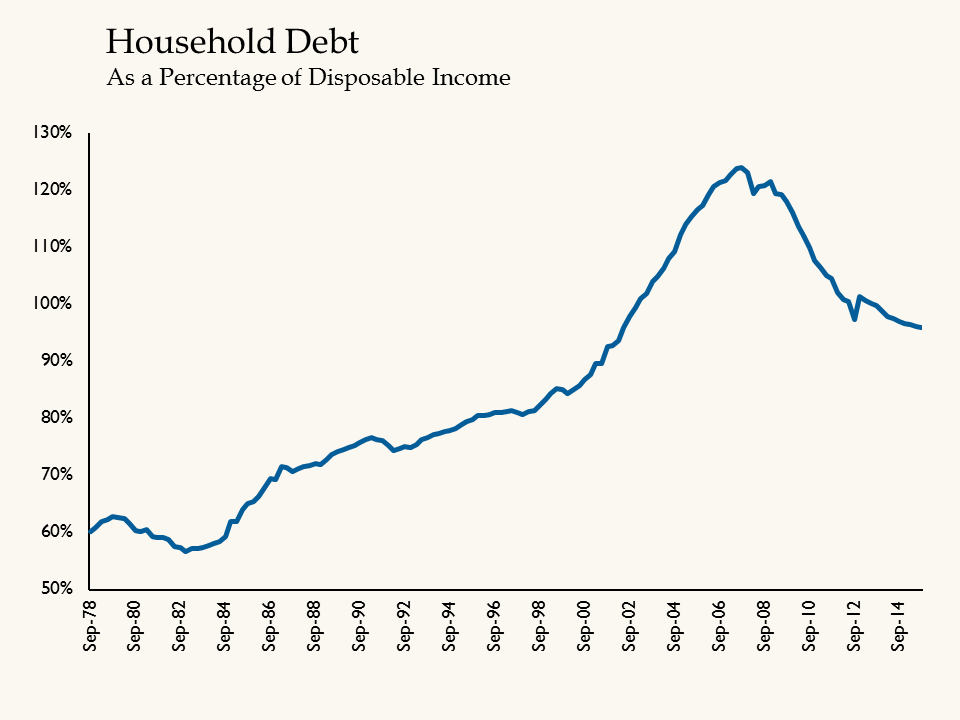

These cheaper borrowing costs, coupled with lower returns in savings accounts, resulted in more debt. Household debt as a percentage of income more than doubled from 1980 to 2007.

Source: FactSet

This was not sustainable; however, it did create a retail infrastructure, which too was extended since it was predicated on individuals spending more than they earned. Therefore, as consumers normalize their savings and debt levels, consumer spending is not going to be as robust as previous decades. However, we believe that this is healthier for the U.S. economy as a whole. Without a doubt, there will be winners and losers as we invest in this age of the “smarter” consumer.

The Coin FlipFrom the global economy to what’s happening here in Oregon

With the improvement in the economy and consumer confidence, local governments went to the ballot box in Oregon on primary day seeking funding. Voters were asked to approve over $890 million in measures, with over 80 percent of these funds allocated to schools.

Not all voters were willing to ante up more. Some major ballots failed in east Multnomah County; Mt. Hood Community College was seeking $125 million and Centennial School District was pursuing $85 million. While the economy in the state of Oregon has seen dramatic improvements, and consumers are better off, raising money at the ballot box is always difficult.

Jason Norris, CFA, is executive vice president of research at Ferguson Wellman Capital Management. Ferguson Wellman is a guest blogger on the financial markets for Oregon Business.