Markets will survive political volatility.

During the past few weeks, we have witnessed a meaningful increase in stock market volatility. Geopolitical tensions, coupled with Washington, D.C. drama around social justice issues, have put investors on edge.

It’s hard reading these headlines. Nevertheless, we believe national and international political developments will not have a lasting effect on the market, and investors will continue to focus on economic and financial fundamentals.

To put the last few weeks in perspective: the headlines could have surely led to a multi-percentage selloff. Fortunately, the market’s reaction was somewhat muted, falling just over 1% the last couple of weeks.

Historically, North Korean headlines have had minimal effect on the stock market. When the country detonated its first nuclear device in 2006, U.S. stocks were actually up. The presidential business advisory councils dissolved earlier this month, yet the markets took it in stride.

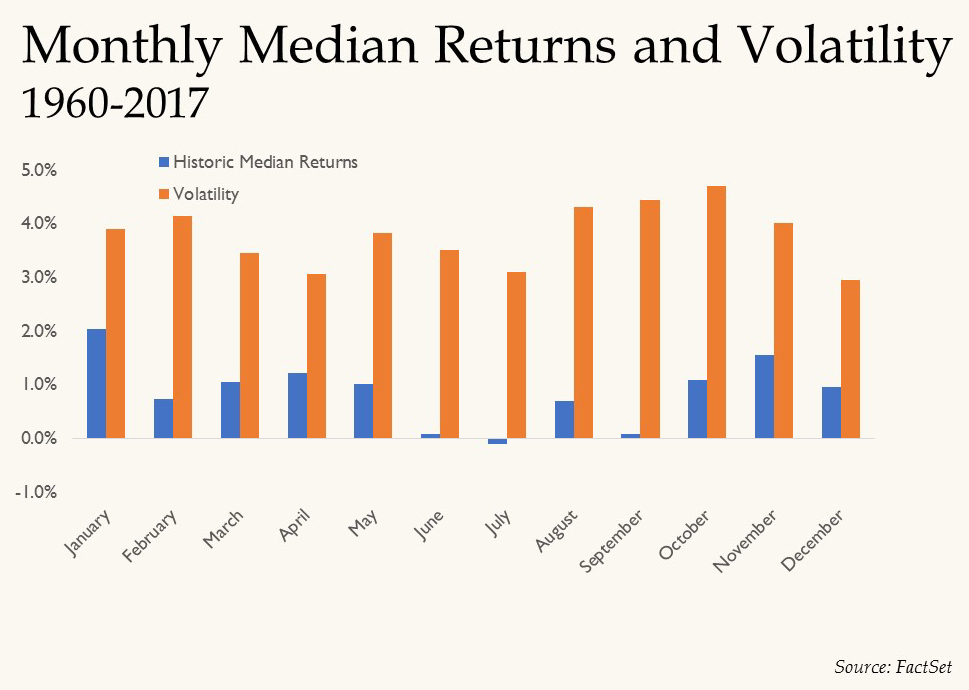

The drawdowns we have seen of late are quite common for the stock market, especially since we are still close to an all-time high. Also, what we see in the summer and early fall often reflects monthly returns and increased volatility, as seen in the chart below.

Volatility in the equity market has been relatively low this year and a meaningful price move was due. In fact, it had been 60 trading days, since May 17 to be exact, that stocks have retreated more than 1%. Stocks have moved up-or-down more than 1% in a day now seven times — only 4% of trading days — this year.

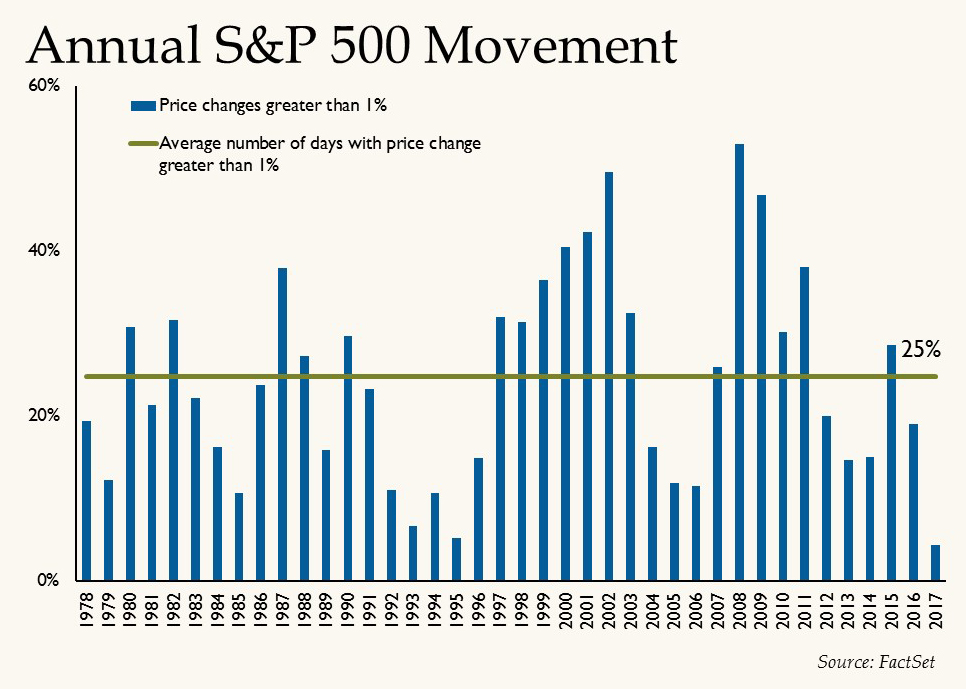

Historically, during any given year, stocks will move more than 1% a quarter of the time, as seen in the chart below.

While all the saber-rattling can be unsettling for the public, it is no surprise that these developments are benefiting defense contractors.

Recent comments from management teams have shown a meaningful increase in interest and orders globally. Raytheon has stated that it is unusual to see such increased demand in multiple regions around the world.

In November 2016, we increased our exposure to defense contractors due to the belief that a Republican-led government would continue increase spending on national security. Recent terror events and North Korea escalations have led to more strength in the sector. When comparing the performance of defense contractors versus the equity market as a whole, defense names are up 33%, compared to 15% growth from the S&P 500 since the election.

Finally, we believe it is too early to change portfolio allocations in light of current headlines regarding the risk of the president not accomplishing his tax reform and infrastructure spending agenda.

We have conveyed to clients throughout the year that this kind of legislation would be frosting on the cake, rather than a critical component of stock growth. Our belief was that economic fundamentals, both domestically and internationally, started to improve over a year ago, thus impacting earnings growth and driving markets upward.

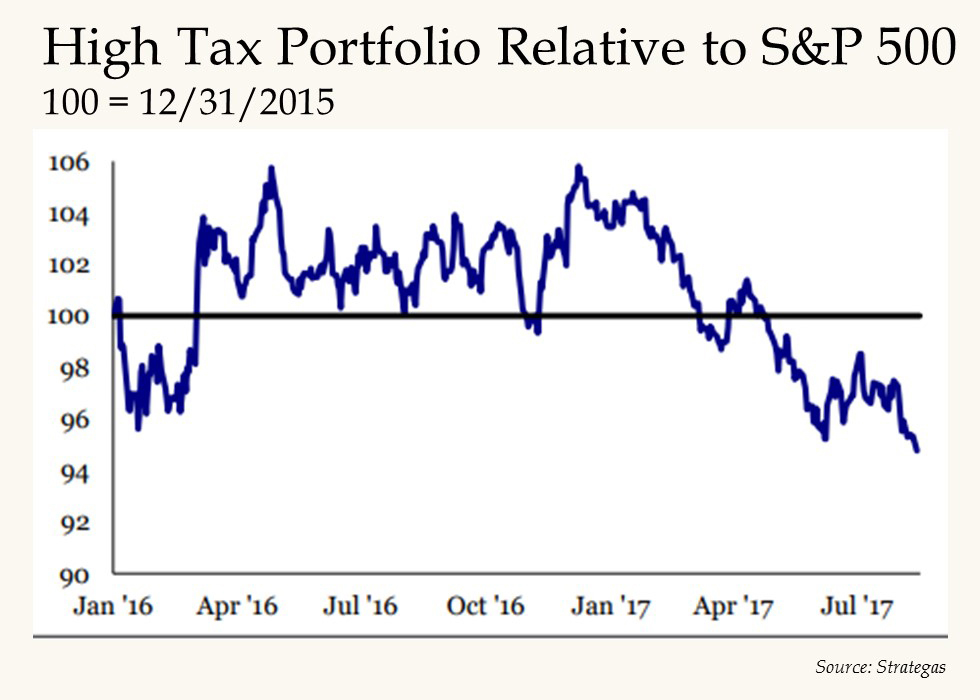

Any bonus on the fiscal side of the equation would simply be … more upside. We believe this is now the consensus in the market, as seen in the following chart from Strategas. Below is an index of companies that would benefit from tax reform due to their relatively high U.S. tax rate.

What stands out for us in this data is the rally this index had following the 2016 election followed by the poor relative performance in the spring when it appeared that tax reform would be delayed. Therefore, any major reform or repatriation would be a benefit to stocks. As we saw on August 22, signals that there may be some tax reform before year-end led to a nice rally in equities, thus confirming that markets are not pricing in tax reform.

Oregon’s Own Chicken Little

One can compare preparing for the worst in the capital markets with what we saw in the days and hours leading up to the eclipse. Oregon Department of Transportation spokespeople sent dire warnings that the coast, I-5 corridor and high desert simply couldn’t handle the potential onslaught of drivers ascending upon our state.

Contrary to predictions, Oregon held her own. Car-mageddon didn’t happen, thanks to communities and businesses stocking up and drivers planning their trips to lighten the load on the roads.

Did this traffic-apocalypse rhetoric save the day or cause unnecessary stress?

We’ll never know, but one could certainly take a similar view with the relationship between news, politics and the markets. Make decisions on facts, not rumors. Plan and prepare early. Stay the course. The future should be bright, with the exception of a few glorious moments of totality.

Jason Norris, CFA, is executive vice president of research at Ferguson Wellman Capital Management. Ferguson Wellman is a guest blogger on the financial markets for Oregon Business.