Uncertainty is the only certainty there is.

John Allen Paulos, professor of mathematics at Temple University, coined this timely phrase that is the topic of this month’s Oregon Business blog. We certainly agree with his sentiment.

Markets dislike uncertainty. In the current economic and political environment, that seems to be the only certainty. As we head into the last two months of the year facing what many pundits describe as an “unprecedented” election, where does it make sense to invest?

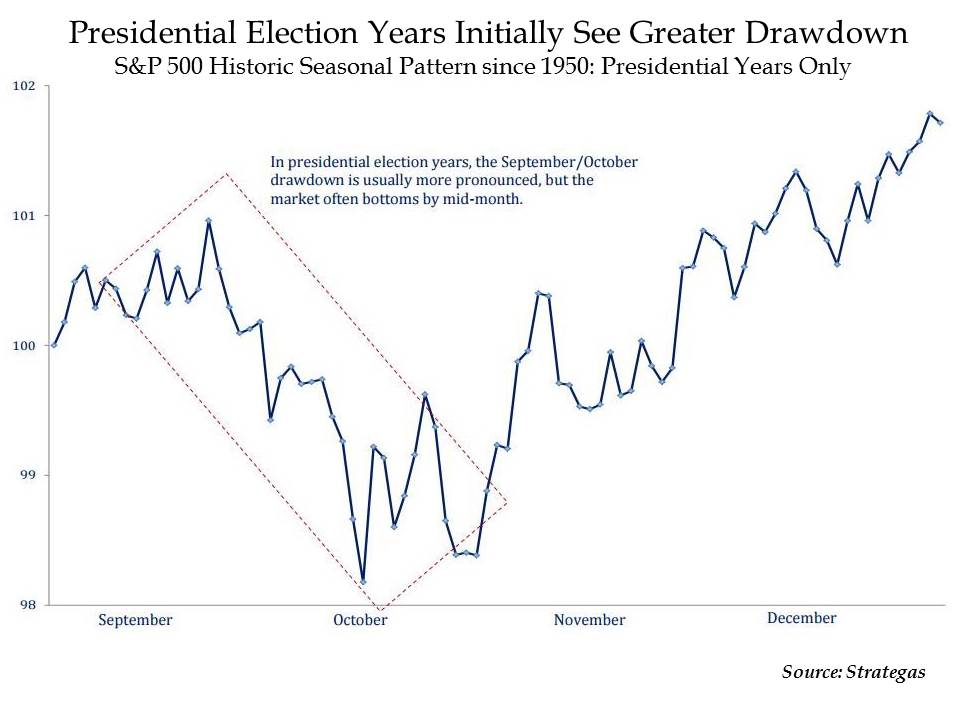

We recently reduced our equity exposure to “neutral” and added to bonds, not with the intention of turning bullish on bonds, but for buying some volatility insurance. Looking back to 1950, stocks usually perform well in these periods. The chart below highlights the average return of the S&P 500 during the fourth quarter in a presidential election year.

Weakness in the first part of October seems to be the norm with a little bounce back in the last 10-plus weeks of the year. While this is only an average, at least history is on the side of remaining long on equities.

Weakness in the first part of October seems to be the norm with a little bounce back in the last 10-plus weeks of the year. While this is only an average, at least history is on the side of remaining long on equities.

Our base-case scenario for the election is that Democrats keep the White House and take the Senate by a slim margin, with Republicans retaining the House. In this scenario, we would expect equities to hold up well and not lead to a major selloff. Investors like gridlock and in this scenario, gridlock will certainly remain.

A risk to our forecast is that in recent weeks, there is an increased likelihood that Republicans will lose the House. This view has been a headwind to the healthcare sector of late, making this the weakest sector over the last month.

Should the White House, Senate and House be in Democratic control, regulatory risk in the healthcare industry would increase. This has spooked investors, resulting in a selloff in the space.

The other headline risk has been Proposition 61 in the State of California. If passed, it would require state agencies (e.g., Medi-Cal) to purchase drugs at or below the price that the U.S. Veterans Administration (VA) receives, which is usually the lowest price. If this passes, and current polls are pointing that way, other states may take on the initiative.

Our view is that this will not have a major impact on the drug sector as a whole and will only have minimal downside to those companies with considerable exposure to state agencies. These companies will look to raise prices elsewhere, such as private insurers and the VA, and possibly limit drugs sold to those institutions as well. This also occurred in 1991 when Congress passed a law requiring drug companies to give discounts to state Medicaid buyers. Prices went up elsewhere, including the VA.

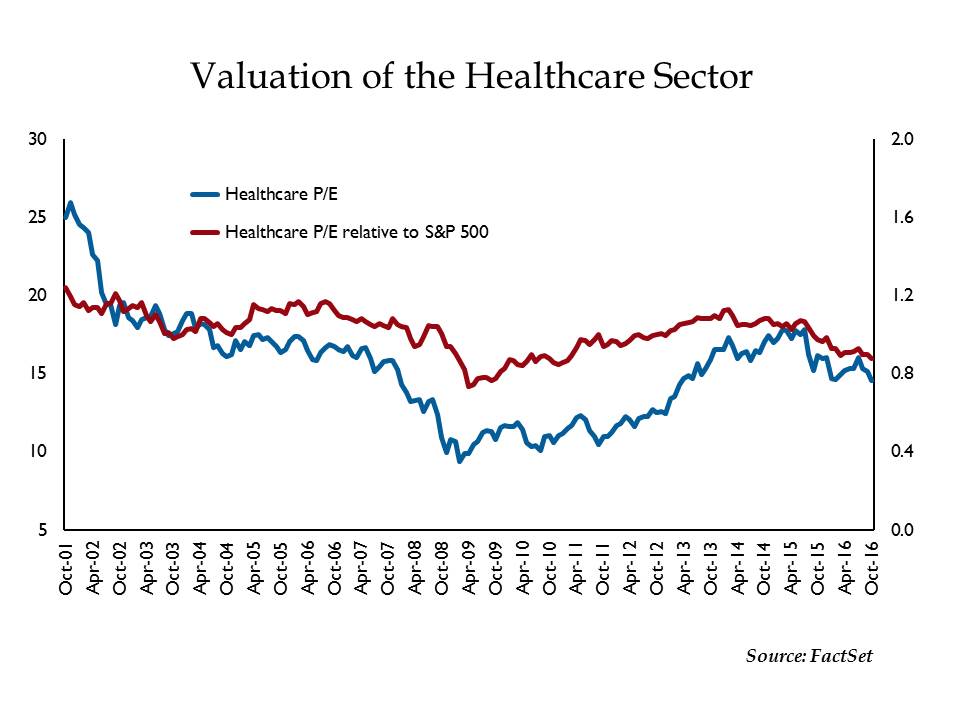

While we are wary of the headline risks, we still believe it is too early to sell stocks and maintain a meaningful exposure to healthcare through an overweight to the benchmark. Historically, healthcare stocks earn a premium valuation (i.e., price/earnings multiple) to the broad market. The chart below shows that with the sector now trading under 15x earnings and a 10 percent discount to the market, healthcare is at the “cheaper” end of its historical range. This sector hasn’t been this affordable since the uncertainty surrounding the Affordable Care Act in 2009.

Attractive valuation coupled with above-average growth prospects underpin our enthusiasm for the healthcare sector at this time. Earnings growth for the S&P 500 is roughly 1 percent for 2016 while the healthcare space offers just under 10 percent growth. As such, with the stocks at a discount to the market, we continue to view the healthcare space positively.

The Coin Flip: From the global economy to what’s happening here in Oregon

While healthcare is often positioned negatively in the headlines, there are groundbreaking products that continue to leave the pipeline and enter the market. In late December, drug maker Eli Lilly will report data from a study regarding Alzheimer’s disease. Their drug is designed to modify the progress of the disease.

Biogen and Merck are also developing similar drugs, but this will be the next major data point in the efficacy. As the U.S. population ages, increasing numbers will be diagnosed with the disease.

In Oregon, Alzheimer’s disease is the sixth leading cause of death and our state has the tenth highest Alzheimer’s death rate in the U.S. If one of these companies can show a significant breakthrough, it would be a major game changer.

**Strategas, RBC Healthcare Research and Alzheimer’s Association were sources for this piece

Jason Norris, CFA, is executive vice president of research at Ferguson Wellman Capital Management. Ferguson Wellman is a guest blogger on the financial markets for Oregon Business.