Political uncertainty has yet to translate into market uncertainty.

Talking heads on cable news as well as in print have painted the picture of a highly uncertain environment. Though this is fairly typical around elections, it is a bit more “noisy” than in the past.

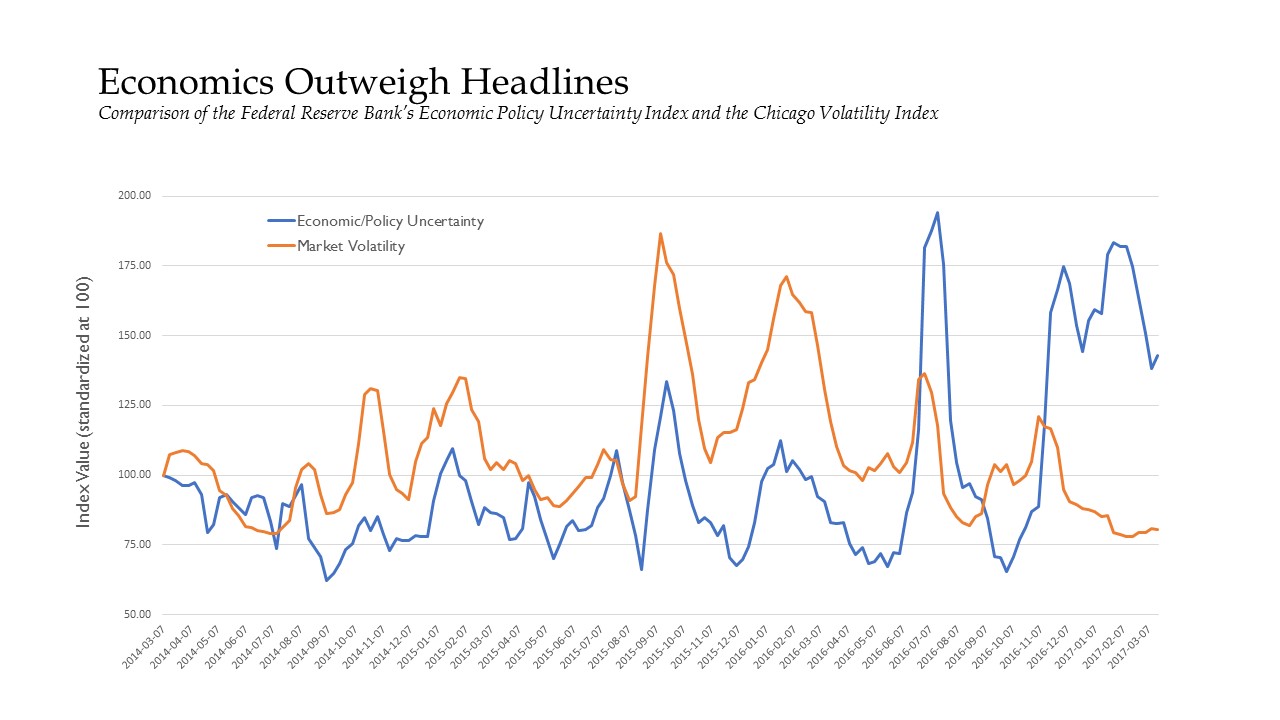

What has surprised us, as well as most investors, is not only the lack of volatility in the markets, but also the money investors have made since the election. The chart below shows the historic correlation between economic/policy uncertainty with equity market volatility — and the lack thereof in recent months.

Generally, as uncertainty in the economy and/or with federal policy increases, it has an effect on the equity markets. What we’ve observed since the election spike in uncertainty, markets have remained complacent and continued to grind higher.

While some investors have contributed to the anticipation of a “business-friendly Beltway,” we believe this is primarily a reflection of accelerated global growth, which hasn’t been a prominent headline.

Bill Gates summed it up best, “Headlines, in a way, are what mislead you because bad news is a headline and gradual improvement is not.” We believe the global economy is improving, and thus would continue to recommend equity exposure.

Repeal and Replace

The Republican House presented their plan, called the American Healthcare Act (AHCA), which is designed to repeal and replace the Affordable Healthcare Act (aka Obamacare).

As an aside, a large percentage of the public did not know that ACA and Obamacare were the same, so perhaps the Democrats may add to the confusion as they develop a name for this new plan. As we look at the current proposal, we do not see it significantly impacting the healthcare sector from an investment standpoint.

Hospitals will face a major headwind as the number of insured declines and bad debts for hospitals increase. It tends to be easier to collect a payment from an insurance company than an individual, hence it being categorized as “bad debt.”

Although our concern going into healthcare reform was focused on drug pricing, there doesn’t seem to be any restrictions in this bill because House Republicans are attempting to get it approved through budget reconciliation, which would require at least 50 votes in the Senate and the vice president breaking the tie.

This approach means that bills can only be introduced that don’t increase the deficit. Therefore, legislation on drug pricing, drug reimportation or any health insurance changes such as selling across state lines will have to be introduced in another bill.

This healthcare legislation needs to withstand a filibuster or 60-or-more votes, which will be much more difficult to pass in a divided Senate. If healthcare stocks do start to sell off in reaction to headlines, we would be inclined to buy as a reflection of our belief that the long-term fundamentals for healthcare remain strong.

Oregon May Need Some First Aid

Oregon has the potential of facing meaningful challenges if the House version of the AHCA is signed into law.

The expansion of Medicaid in the state over the last several years reduced Oregon’s uninsured to 7%, which is below the national average, and Medicaid coverage expanded by over 65%.

The state has been dependent on a federal grant of $1.9 billion and over time, the matching grant has been reduced, putting the state in a deficit of $700 million. With the House plan, Medicaid reimbursement will continue to decline, which will put the state in a large predicament. In short, expect more tax proposals to come out of Salem to fund this growing gap.

Jason Norris, CFA, is executive vice president of research at Ferguson Wellman Capital Management. Ferguson Wellman is a guest blogger on the financial markets for Oregon Business.