Would Oregon benefit from a state-owned bank? As small businesses struggle, the idea is debated on Main Street, in Salem and by the banking community.

By Ben Jacklet

Between October and December of 2010, a team of researchers went door-to-door canvassing Main Street businesses from Ashland to Troutdale. The goal was to get a sense of the credit challenges facing small businesses and farms, and to gauge potential support for a state-owned bank to boost lending in Oregon.

The survey was not scientific. “I basically walked down the street and if the business was open I talked to them,” says Dan Lombardi, statewide small business organizer for the Main Street Alliance of Oregon.

Nor was the study objective. The Seattle-based national organization backing the research project, Alliance for a Just Society, is an advocacy group formed to support President Obama’s health care reform bill.

But the findings of the January 2011 “Direct from Main Street” report were compelling. More than half of the 116 Oregon-based business owners and farmers canvassed said they had struggled to get loans. Two-thirds of those who struggled to get loans said they had delayed expanding as a result. An even greater majority — 75% of all those surveyed — supported the creation of a state bank in Oregon.

What is a state bank and how might it look in Oregon?

There is only one state bank in the nation, the Bank of North Dakota. It was established in 1919 to give farmers more control and greater access to capital. Ninety-two years later it has evolved into a 170-employee institution with $4.2 billion in assets and an impressive record of performance. “We’ve had record profits for seven years in a row,” says bank president Eric Hardmeyer.

There is only one state bank in the nation, the Bank of North Dakota. It was established in 1919 to give farmers more control and greater access to capital. Ninety-two years later it has evolved into a 170-employee institution with $4.2 billion in assets and an impressive record of performance. “We’ve had record profits for seven years in a row,” says bank president Eric Hardmeyer.

Hardmeyer has run the bank for the past 10 years. As an indication of the importance of his role, his predecessor John Hoeven left to become first governor and later U.S. Senator.

Hardmeyer explains that the Bank of North Dakota is funded through captive deposits. All taxes and fees collected by state government funnel through the treasury into the state bank, rather than going out to bid with private banks. The state bank uses that money to fund state services and manage a $2.8 billion loan portfolio, partnering with community banks in the private sector to boost agriculture and small business.

If that sounds like socialism, well, it kind of is. And it has worked. North Dakota has the lowest unemployment rate in the nation. Property values did not fall there during the housing crash. The bank transferred $340 million back to the state in dividends over the past dozen years, but has not contributed any money for the current biennium because, amazingly, it is not needed. While Oregon and other states are struggling with billions of dollars in shortfalls, North Dakota enjoys a budget surplus.

Given those results, it isn’t surprising that hard-hit states are considering state banks. But just as there is only one Bank of North Dakota, there is only one North Dakota: population 650,000, with significant oil and gas reserves. The state’s success probably has more to do with hydrocarbons than fiscal policy.

Hardmeyer is quick to clarify that he doesn’t recommend that other states try to replicate his bank’s model. Asked what advice he has to offer to states considering it, he says: “You’d better staff it with bankers, not economic development folks. Or else you will have a very expensive, short-lived experiment… The other issue is to make sure you aren’t competing with the private sector.”

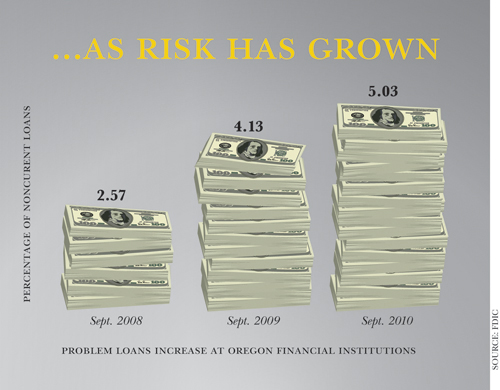

Community bankers in Oregon worry that a state-run bank would do just that. “The idea that the state would become a behemoth competitor would be very concerning to me as a community banker,” says Cort O’Haver, executive vice president of commercial banking for Umpqua Bank. Umpqua, the largest Oregon-based bank with $12 billion in assets, increased commercial loans by 23% in 2010 after a big drop-off in 2009, and recently launched a new business banking division to increase lending further. But data from the FDIC shows that financial institutions have cut back on lending over the past several years as problem loans have grown.

Linda Navarro, CEO of the Oregon Bankers Association, says the Bank of North Dakota resulted from a “quirk of history” that has little to do with modern realities. “For most community banks, the crux of their business is commercial lending,” she says. “They are looking for good business loans to make… They just need to make sure the loans can be repaid.”

Bill Humphreys, CEO of Corvallis-based Citizens Bank, says he has studied the North Dakota model and concluded that a state bank would be against the interests of the state and taxpayers. “I don’t see how a state-owned bank could enter the marketplace and all of a sudden start making loans that aren’t being made now,” he says. “Unless they decide they’re going to take on greater levels of risk.”

Humphreys and other bankers point out that one driving reason behind the financial meltdown was loose, easy credit without proper collateral. A state-run bank committed to lending to businesses would “share the consequences of higher risk with the taxpayers,” Humphreys says. “This is not a good time to do this. If you look at the state as a business, they are in such a deficit position that they have no business investing in anything.”

But opposition from bankers hasn’t stopped small-business owners from organizing. A coalition of 500 small-scale business owners and farmers led by Jim Houser of the Hawthorne Auto Clinic in Portland and Mark Kellenbeck of Cascade Management in Grants Pass has formed to promote the idea. Supporters have organized boisterous public hearings to make the case that a state bank would put taxpayer money to work for Oregonians.

But opposition from bankers hasn’t stopped small-business owners from organizing. A coalition of 500 small-scale business owners and farmers led by Jim Houser of the Hawthorne Auto Clinic in Portland and Mark Kellenbeck of Cascade Management in Grants Pass has formed to promote the idea. Supporters have organized boisterous public hearings to make the case that a state bank would put taxpayer money to work for Oregonians.

Roughly 150 people attended one such forum in Northeast Portland on Feb. 1. Audience members voiced support for the idea and empathized with small-business owners and farmers denied loans due to their size. The prevailing themes of the speeches made by both the audience and panel were the pervasive lack of credit available to small-business owners and small farms, how to fund and structure a state bank, and why Oregon needs one.

“One of the things about the state bank is that it is not not-for-profit, but that the profit belongs to the people,” said Barbara Dudley, co-chair of the Oregon Working Families Party. Dudley told the crowd that the bank could not only provide money to businesses that need capital, but could also become a viable revenue source for the state.

To become a source of revenue rather than expense, the state would have to choose its loans carefully. Several major state loans have failed magnificently in recent years, such as the $20 million loan extended to the now-bankrupt Cascade Grain ethanol plant in Clatskanie.

One of the small businesses featured in the Main Street report is Allegri Wine Shop & Art Gallery in downtown Gresham, in a neighborhood that recently lost a bridal shop, a toy shop and a bike shop. Owner Bill Allegri says he has been unable to get a bank loan, so he’s had to refinance his home and reduce inventory. His original business plan called for hiring an employee to enable him and his wife Kathy to travel to wine regions and build relationships with winemakers to grow the business. Instead they have done “what needs to be done,” including going without health insurance. “Fortunately we have good health,” he says.

Allegri says he is not very familiar with the North Dakota model of a state bank, but he would support “any financial institution open to listening to small businesses to see how they could help them.”

Another supporter is Barbara McLean, who runs the One Stop Sustainability Shop in Northeast Portland with her daughter Jessica Ilalaole. They have struggled since launching in December 2009 with the goal of providing affordable everyday products to help people live more sustainable lives. Their shelves are stocked with dustpans made from recycled plastic, envelopes layered with old newspaper instead of bubble wrap and handmade soaps.

But it’s hard to pay the bills with idealism. After failing to get a loan through her credit union, McLean took out a home equity loan. She and her daughter moved from the pricey Pearl District to funky Alberta, where they’re hoping business will pick up as the weather warms. “We’d like to pay ourselves at some point,” says Ilalaole. Later in the interview, she mentions matter-of-factly that the shop’s unusual prices date back to the launching of the business, when “we didn’t know what we were doing.”

That offhand admission brings up an important point. Prior to opening his wine shop, Allegri worked for 25 years at a nonprofit. McLean’s previous work was doing fish surveys in the North Fork of the John Day River. Both followed their dreams to launch Main Street businesses, but their companies have not grown organically.

North Dakota’s Eric Hardmeyer says a state-run bank must avoid the temptation to loan to every business that needs cash with the hope that it will succeed. “You can’t save every deal,” he says. “You can’t save every town. Some deals you just have to walk away from.”

State legislators haven’t walked away from the ambitious project of establishing a state-run bank from scratch in Oregon. They’re running away from it. A bill introduced this session by Rep. Bob Jenson (R-Pendleton) calling for a North Dakota-style bank quickly morphed into a compromise proposal for an “Oregon Financing and Credit Authority” backed by Rep. Phil Barnhart (D-Eugene) with support from State Treasurer Ted Wheeler. Business groups such as the Oregon Business Association and Associated Oregon Industries have not yet taken a position on the issue.

The still-evolving compromise proposal calls for consolidating existing programs and funds rather than creating a new state bank. “We’ve spent a lot of time looking at how to use the assets we already have in a more productive way,” says Barnhart. “We could invest some of that money in lending to small businesses to build Oregon’s economy.”

Wheeler, whose role would change radically under a state bank system, says it makes sense to combine the state’s economic development offerings into one office that also participates in loans originated by local banks rather than competing with those banks. “We don’t need to replicate the North Dakota model,” Wheeler says. “I don’t think it would be a good use of public funds, and I don’t think it’s necessary. We can leverage off of the things already in place and achieve the same goals.”

For example, in late January Wheeler’s office reduced collateral requirements for banks that receive public fund deposits from 100% to 75% as a reflection of the improved economy. That freed up an estimated $600 million for local lending without costing taxpayers anything.

Wheeler says improving other existing programs and policies could bring similar results. He has shared his ideas with the bankers association and the Working Families Party, and the ironing out of details is under way.

The end product, should it become law, will probably share little in common with the much-idealized and feared Bank of North Dakota. It will not require the immediate hiring of bankers for state jobs. Nor will it endanger the liquidity of public funds or sap money from the general fund in times of intense cost-cutting. Wheeler, Barnhart and other supporters of the middle way are hoping it will help solve the credit problem without creating a fresh supply of new problems. Time will tell how deep their support reaches in a legislative session already packed with challenges.

Oregon Business writer Peter Beland provided reporting for this article.