BY JASON NORRIS | OB GUEST BLOGGER

BY JASON NORRIS | OB GUEST BLOGGER

Active vs. passive investing: what you need to know.

BY JASON NORRIS | OB GUEST BLOGGER

Active vs. passive investing: what you need to know

Jack Bogle is on Cloud Nine. The biggest proponent of passive investment management and founder of Vanguard saw over $200 billion of inflows from investors in 2014 as frustration increased with active management. Depending on asset class, 75 to 90 percent of active managers trailed their benchmark in 2014.

Before we dive into the active-versus-passive argument, here is a brief synopsis of the two strategies, although the difference between the two can be very fluid.

The rise of passive investing started with bull market in the 1990s. Investment managers were struggling to keep up with their benchmarks; therefore, investors took the belief that if they can’t beat them, join them. For example, rather than buying a mutual fund that purchases stocks and attempts to deliver returns greater than the S&P 500, why not buy a mutual fund that tracks the S&P 500? The argument went, if less than 50 percent of investment managers cannot deliver returns better than their benchmark, just buy the benchmark.

This is the heart of passive investing. The previous example is a simple one, because when investors add different asset classes, such as bonds or international stocks, there can be an active component regarding how much to own and when to rebalance. When it comes down to it, passive investing is buying the “benchmark” and giving up the opportunity for to perform better, while “guaranteeing” not to perform worse. Passive investments sometimes have lower fees than active investments; however, these fees virtually guarantee the investor will receive returns lower than the benchmark.

Which is the best approach? It depends. As we saw in 2014, passive investing did meaningfully better than active. While this lack of alpha is a concern, it is not the most important contribution to an investor’s overall return. The biggest factor is the allocation between stocks and bonds, and then which equities are favored, such as large cap, small cap or international. The U.S. large cap space was the best game in 2014, and the more exposure the better for investors.

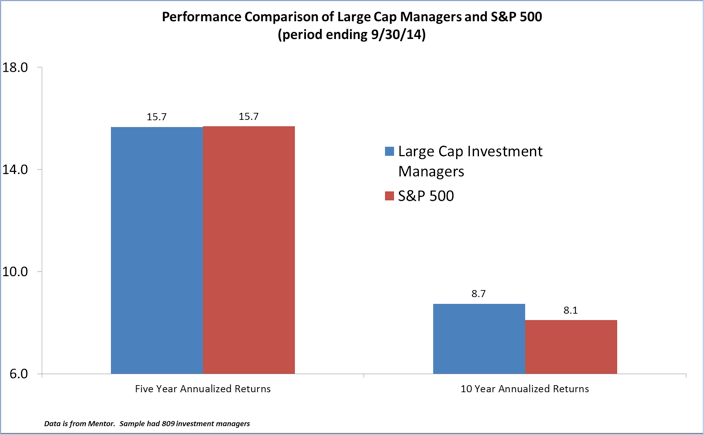

There will be periods when passive outperforms active; however, over longer periods of time, active has shown to be superior. Over the past five years 50 percent of institutional active managers outperformed and over the past 10 years that 75 percent of active managers have outperformed. Chasing last year’s performance has never been the best policy. The key for investors is patience.

The purpose of the chart is to provide comparative results of broad-based market indexes. There is no relationship between Ferguson Wellman and the market indexes. The comparison indexes do not report net returns.

Fees are another consideration, and for the most part, active managers do have higher fees, however, passive investment managers assess fees on top of the passive funds they are using.

With both approaches investors need to be knowledgeable of all the fees they are paying, both direct and indirect. When choosing an investment manager or mutual fund, due diligence is key. Assessing longer term returns for the entire portfolio should be the main consideration.

The Coin Flip

From the global economy to what’s happening here in Oregon

There are three Oregon investment managers and four large-cap strategies from the Mentor database we used to get our results. Over the 10- year time period, all four of the large-cap strategies outperformed the S&P 500.

There are also a number of passive investment firms that had a good year in 2014. Regardless of your investment philosophy, there are some high quality firms to choose from here in Oregon. What is key to achieving your retirement goals is putting your money to work, not sitting on the sidelines just watching the headlines.

Jason Norris, CFA, is executive vice president of research at Ferguson Wellman Capital Management. Ferguson Wellman is a guest blogger on the financial markets for Oregon Business.