I don’t think anyone can (or should) remember what it was like to get things done without the internet. This milestone in technology has certainly benefited brick-and-mortar companies and subsequently launched a new era of businesses.

BY JASON NORRIS | GUEST BLOGGER

A Silver Anniversary

Former Vice President Al Gore’s pride and joy turned 25 in March and I don’t think anyone can (or should) remember what it was like to get things done without the internet. The productivity enhancements for the global economy have been tremendous and continue to make the world “flat”— a term coined by Thomas Friedman back in 2005. This milestone in technology has certainly benefited brick-and-mortar companies and subsequently launched a new era of businesses.

The first wave we experienced occurred in the late 1990s. Any business that incorporated a “.com” after its name was able to increase its value meaningfully, even though profits were last thing on investors’ mind. While many of these companies have come and gone, they have set the stage for a major build out of infrastructure that has changed the way the world works and plays. While the memories of those internet bubbles of the late 90s have either popped or floated away, some recent activity in the social media space is starting to feel like “déjà vu all over again.”

King Kandy

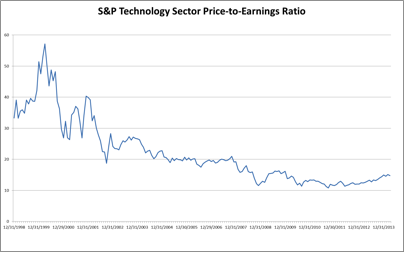

Market pundits recently have pointed to IPOs of late, such as Facebook and Twitter, as a sign that we are reliving the late 1990s again with respect to “internet” stocks. While valuations for some companies may be bit excessive, this phenomenon is a narrow portion of the market, whereas in the late 90s, large-cap tech was enjoying the bubble as well. Remember when Cisco Systems was close to a $500 billion company? The valuation of the sector today is still meaningfully below what we saw 15 years ago (see chart). The price-to-earnings reached a bubble peak of just under 60x, where today the sector is trading at roughly 15x earnings, which is below that of the broad market.

Soon we will witness an IPO from online game maker King Enterprises, developers of the hit game Candy Crush. While the valuation on the surface doesn’t seem too high, (9x EBITDA), if you look at another one-trick-pony called Zynga, which has a certain game on Facebook called Farmville, that cash flow may not be too sustainable.

Source: FactSet

Private Eyes

I recently attended a panel discussion involving six major private investors at a technology conference hosted by Morgan Stanley. These investors covered all levels of the spectrum from early stage angel investing (see Ralph Cole’s article for a further description) to pre-IPO funding rounds.

Participants stated that they believe we are in a 15-year peak of the number of businesses generating losses and Silicon Valley entrepreneurs have no institutional memory of internet bubbles of 1999 and 2000. Also, they believe there is a lot of “froth” in the market at all stages; however, the pre-IPO round seems to exhibit the most hype. One reason is that considerable public money is able to participate in these rounds, thus attracting for funds. These investors seem to just focus on revenue growth and not understand the dynamics of the business model. This easy access to capital is also bringing change to composition of the board of directors. As more “investors” gain board access, the objectives for the company become compromised. Investors are looking at when they can monetize their stake rather than the long-term strategic vision of the company they are investing in.

The businesses that investors are focusing on are in the software and mobile space. They believe that hardware is too commoditized and therefore difficult to make money. Within software, security and data analysis are keys to success. Allowing businesses to manage their data and track their customers’ patterns and routines is an opportunity for new software developers.

What does this mean for the public markets and tech investing? Be selective. We are seeing a number of products pushing costs down, which is great for consumers, but may not be the case for vendors. We continue to focus on the mobile market, as well as software and security in the Cloud. We believe tech spending, globally, should recover; however, we continue to see weakness in emerging markets. Therefore, we remain slightly underweight the benchmarks in our allocation to technology stocks.

Spring Forward, Bracketology and Lost Productivity

During this time of year, you may ask yourself: Is technology a friend or foe of business?

According to a recent article in Business Insider, productivity is impacted by moving our clocks forward in the spring. An estimated $2 billion in lost productivity has been calculated due to lack of sleep and the potential for “cyberloafing,” which is the activity of passively searching around internet rather than working during the day.

Then shortly after daylight savings, we welcome March Madness. Again there are a many studies regarding how American workers become unproductive during those first two days of the tournament. A research firm called Challenger Gray has estimated that roughly $135 million will be lost in wages due to people focusing on their early round upsets rather than work. This may be overstated; however, anecdotally many of us do get caught up in the “madness.”

Fortunately, the American worker is has become accustomed to multitasking. For those filling out a bracket this year, good luck and hopefully your IT departments don’t have restrictions on streaming abilities on your computer.

How the Heck to Value Tech

When investors look at technology stocks, several different valuation metrics are used. Some of the most common are price-to-forward earnings, price-to-sales and enterprise value to EBITDA. These metrics bring more or less value to the analysis based on where a company is in its lifecycle. Investors will typically usually use price-to-sales when a company is early in its lifecycle and price-to-earnings for more “mature” names. We prefer to use the EV/EBITDA metric because it encompasses some balance sheet items and excludes any non-cash expenses on the income statement. We acknowledge there is not a perfect tool. That is why investing is both an art and a science.

Price-to-sales (P/S): total market value divided by revenues

Price-to-earnings (P/E): total market value dividend by net income (or stock price divided by earnings-per-share)

(EV/EBITDA): Total market value (or enterprise value) plus debt minus cash dividend by earnings before interest, taxes, depreciation and amortization

Jason Norris, CFA, is executive vice president of research at Ferguson Wellman Capital Management. Ferguson Wellman analysts blog on the financial markets for Oregon Business.

Disclosures:

Opinions and statements of financial market trends based on current market conditions constitute our judgment and are subject to change without notice. Due to the rapidly changing nature of the financial markets, all information, views, opinions and estimates may quickly become outdated and are subject to change or correction. We believe the information provided is from reliable sources but should not be assumed accurate or complete.

Reference to or by non-employee individuals and institutions herein does not serve as an endorsement of, or testimonial for, Ferguson Wellman’s investment strategies and services. The information published herein is provided for informational purposes only, and does not constitute an offer, solicitation or recommendation to sell or to buy securities, investment products or investment advisory services. Nothing contained herein constitutes financial, legal, tax or other advice. The appropriateness of an investment or strategy may not be suitable for all investors and will depend on an investor’s circumstances and objectives.