After decades of prioritizing mortgages and car loans, Oregon’s consumer banks are shifting focus. How can they compete in a high-interest world?

Oregon’s consumer banks have been through it.

Back in the early, foggy days of the COVID-19 pandemic, bankers were frontline heroes, working nights and weekends to process 115,874 Paycheck Protection Program (PPP) loans. This federal lifeline infused Oregon’s businesses with over $10 billion in forgivable loans.

Those funds, and money from other COVID-19 programs — remember those sweet, sweet stimulus checks back in 2020 and 2021? — landed right back at the bank, pushing deposits to historic highs. Rock-bottom interest rates, the norm since the Great Recession of 2008, continued to spur lending as clients took out mortgages, dipped into their home’s equity and financed cars with basically free money.

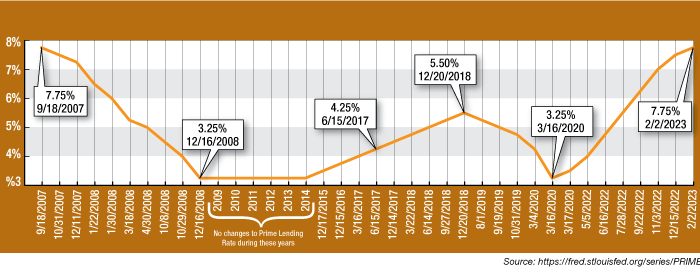

Today’s banking landscape looks very different. Interest rates keep spiking higher and higher as the Federal Reserve works to cool rampant inflation. Yet inflation continues to sizzle, rising to 6.4% in January 2023. With inflation that high, experts predict the Fed will keep the prime rate up for at least a while.

“I don’t know of any forecast that shows a substantive reduction of rates,” reports Roger Busse, James F. and Shirley J. Rippey Professor of Practice at the University of Oregon’s Lunquist College of Business. “Most outlooks show a bank prime rate no lower than4.75% to 5.75% over the next two years. The current bank prime rate is 7.75%.” [Editor’s note: As this issue went to press, the Federal Reserve increased the reserve rate to 4.9% and the published prime rate was 8%.]

This challenging environment puts pressure on consumer banks to grow deposits, as some experts fear a decline in deposits could put pressure on loan-to-deposit ratios, a key metric of bank liquidity. It may not be easy. Customers without much disposable income dipped into saved deposits long ago to make ends meet. Those with deeper pockets are on the move, shopping their money around to find the best financial product with the highest interest rates.

All of this comes at a time when consumer banks face other disruptions like the threat of consolidation, pressure to close expensive branches and the rise of Buy Now, Pay Later plans that could cut into the traditional credit card offerings. How will Oregon’s consumer banks survive?

“This has certainly been a very interesting time for bankers,” admits Tiffany Washington, executive vice president of finance and operations at SELCO Community Credit Union. “Those last couple of years really grew our deposits.”

Washington notes that in an ideal world, the loan-to-deposit ratio is between 85% and 88%. “That’s a really nice spot, but it rarely happens. Usually, we’re either in a deposit market or loan market.”

Shifting to a deposit market means Oregon’s banks now fiercely compete for funds with many different entities. Depositors can choose Treasury Bills from the federal government, insured Certificates of Deposit (or uninsured CDs for the bold) and High-Yield Savings Accounts. Online banking makes researching products and moving money seamless — no appointments with a banker required.

“The environment is much more commoditized than it used to be,” Washington says. “People used to value a banking relationship, but that is not necessarily the way they want to operate now.”

Of course, even the most mission-driven banks and credit unions offer online platforms for virtual banking, but they still lean hard on that face-to-face personal connection.

Craig Wanichek, president and CEO Summit Bank in his office in downtown Eugene

Craig Wanichek, president and CEO Summit Bank in his office in downtown Eugene

“Bigger banks rely on technology and algorithms. We continue to rely on relationships,” says Craig Wanicheck, president and CEO of Summit Bank. (Not a commercial bank per se, Summit is an independent community bank focused on business banking services.) “We stress that a deposit in our branch gets turned into a local business loan.”

Washington also stresses the importance of the personal touch. “Sure, a large segment of the population wants online and self-serve banking, but we’re a community-based organization. We want to be there for our members, virtually or face-to-face, and reward them for saving.”

But relationships go only so far when better interest rates are just a few computer clicks away. This potential decline in deposits worries some national banking experts, but UO’s Busse remains confident.

“The average and median loan-to-deposit ratio for the [currently] 15 Oregon-headquartered banks is 63.4% and 63.6% as of Q3 ’22, with four of those banks above 80%,” he says. Busse admits that these ratios are lower overall for many of these banks versus their historical experience due to “the flood of deposits arising from the PPP and other COVID-19 programs.”

Busse acknowledges that rising rates and the expected deposit runoff has “raised a lot of attention” but argues that “many of these deposits are excess funds, i.e., funds that are idle and not being employed in core operations of businesses or consumer transactions at banks. The actual number of deposit accounts among banks appears to be remaining fairly steady. At this time, I don’t believe there is risk to Oregon banks based on the loan-to-deposit ratios or liquidity pressures. In my view, they are very well capitalized and liquid overall, but more, they have several funding options if needed, including the Federal Home Loan Bank and other tools at their disposal.”

Good news, but bumpy roads still lie ahead. “We’re expecting some escalation of loan losses,” says Washington. “This is after years of seeing none.” Busse echoes that forecast, predicting the delinquency rate will rise from 2.4% to 2.7% in 2024.

This new inflation/interest rate environment piles on another layer to the challenges banks already face. For instance, consolidations and closures, a trend since the 1980s, continue. The National Community Reinvestment Coalition reports that 9% of all U.S. branch locations closed between 2017 and 2021. The closure rate doubled during the pandemic when 201 branches closed per month.

That trend may or may not continue. “There is continued interest in consolidation, perhaps including some Oregon banks,” says Busse, “but with the current economic environment, it may be difficult to make the acquirer’s purchase price, (and method of purchase, e.g., cash, stock or some combination) — as well as the metrics of combinations beneficial to both parties and their shareholders at this time.”

Still, Busse hedges his bet. “That’s not to say it won’t happen in the next 12 months or thereafter.”

While this leaves a growing number of customers without a nearby brick-and-mortar location, online services continue to grow. The preferred mode of banking for millennials and Generation Z, platforms that offer online banking, electronic payment options, the ability to access funds and make transactions are now must-haves for any bank.

Attracting the next generation of banking customers might require even more. Younger customers look at banking differently than their parents. They are cool with juggling accounts across multiple banks and using Neobanks, which only exist in the virtual world. They are also more likely to use Buy Now, Pay Later services. Akin to rent-to-own and layaway plans of old, the growth of this widely offered service may cut into the lucrative bank credit card market.

“There’s a lot more to concern ourselves with today,” says Washington.

Despite all this disruption, the banks of tomorrow will not be that much different than they are today. Physical locations, for instance, will not totally disappear, according to Busse, but they may change a bit. “Many industry and independent studies continue to show that customers want physical locations where they can meet with bankers if needed,” he reports. “Banks will size their physical locations to ensure clients have face-to-face access as desired, and do studies to ensure they are meeting these needs and serving the communities.”

And the challenging high-inflation/high-interest environment will not last forever. “Every cycle has some nuance,” says Busse, “and we are still facing some headwinds. But Oregon’s banks are better capitalized than they’ve ever been. Their safety and soundness are very strong.”

To subscribe to Oregon Business, click here.