Brand Story – One of Oregon’s Largest Money Managers has Beaten 99% of its Morningstar Category Over the Last Five Years by Investing in Discounted Closed-End Funds.

Introducing: Matisse Capital

An SEC-Registered RIA firm headquartered in Lake Oswego that manages over $1 billion in client assets on a fee-only basis; Matisse’s client base primarily consists of high net worth individuals, foundations & endowments, retirement plans, and institutions throughout the Pacific Northwest.

Historically a value-driven investment advisor that has specialized in traditional mutual fund research and tactical asset allocation, Matisse took a leap seven years ago, launching a niche publicly traded mutual fund that invests in discounted Closed-End Funds, and it might just be the best investment strategy you’ve never heard of. “It didn’t happen overnight,” says Bryn Torkelson, Founder and CIO of Matisse Capital. “This was a natural progression. Our core business had always been traditional mutual fund research and asset allocation. So, we took our core business, and applied it to discounted Closed-End Funds.”

What are Closed-End Funds?

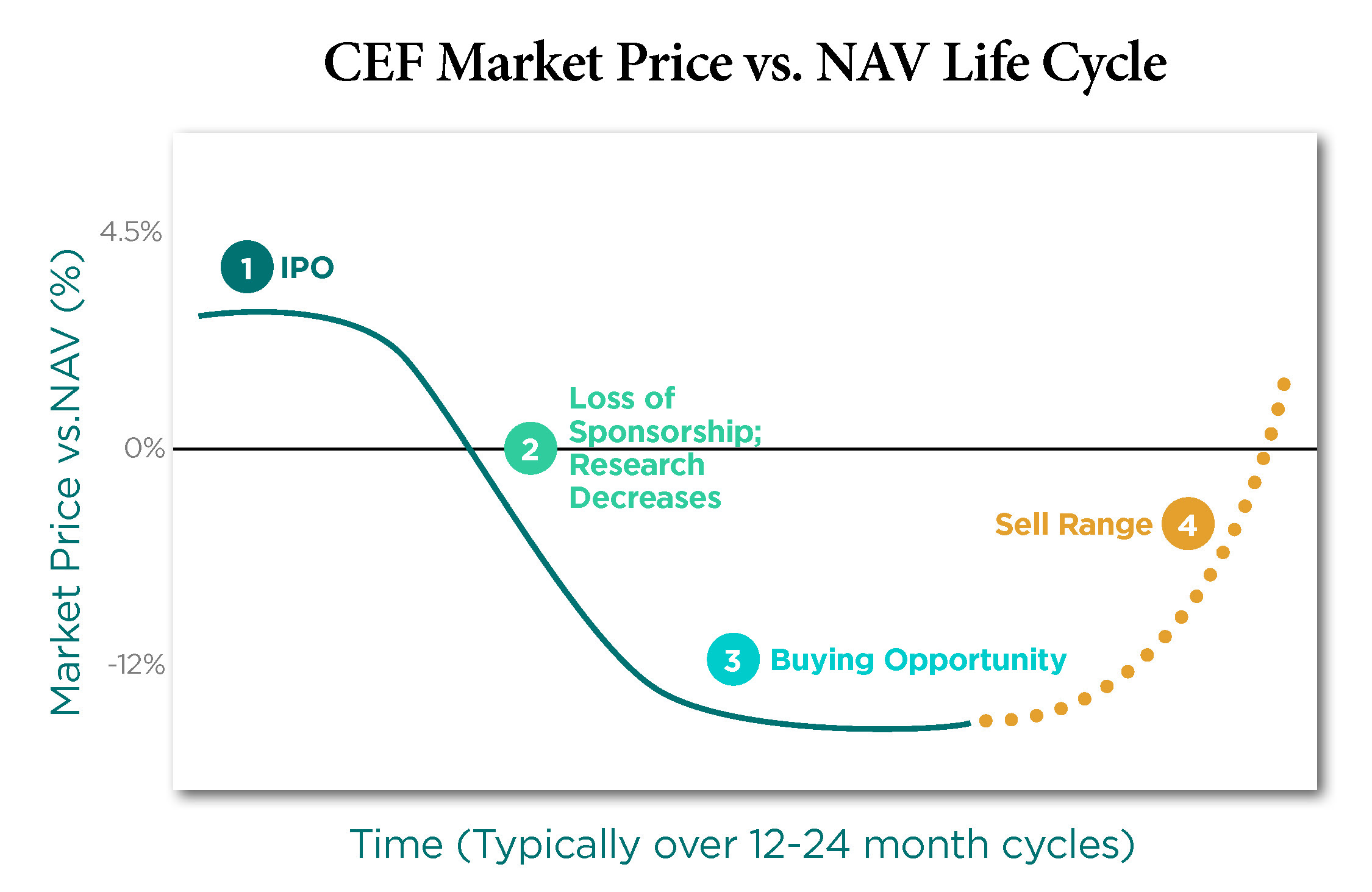

Closed-End Funds are mutual funds with a fixed number of shares. Following a Closed-End Fund’s initial public offering, it does not issue new shares for additional investment. These funds trade throughout the day on exchanges similarly to stocks or ETFs, and their net asset values are published daily at market close.

The market price of a Closed-End Fund, however, is determined by supply and demand. Market forces can cause a Closed-End Fund’s price to vary significantly from its daily reported net asset value (NAV), leading them to trade at substantial premiums (price > NAV) or discounts (price < NAV). Bryn emphasizes that “It’s the only market where you can find high quality mutual funds trading at 85 cents on the dollar.”

Matisse’s investment thesis focuses on Closed-End Funds trading at relatively large discounts. As Bryn explains, “The price of a Closed-End Fund is swayed heavily by supply and demand. We boil it down to investor emotion—fear and greed—which creates opportunities for sophisticated investors.”

Closed-End Funds are nothing new—some have been around since 1893. Yet they have remained largely unknown for two main reasons:one, there are 480+ Closed-End Funds in existence today, with a total market cap of only $222 billion (leaving little incentive for major institutional investors and brokerage firms to get involved); and two, they operate in (what Matisse considers to be) an inefficient market with limited liquidity, information, and analyst research.

“Discounted Closed-End Fund trading isn’t for novices or beginners. It requires disciplined active management with constant tracking and analysis to succeed,” says Nik Torkelson, Matisse Capital’s Vice President of Finance and Marketing.

Vintage baseball photography hangs in the Matisse conference room as an ode to their “singles hitting” approach

Vintage baseball photography hangs in the Matisse conference room as an ode to their “singles hitting” approach

Research Nowhere to be Found, But Too Compelling to Ignore

In the early 2000s, some of Matisse’s clients were asking for income alternatives to bonds and dividend-paying stocks. Matisse began researching and focusing on Closed-End Funds (specifically those trading at discounts), and ultimately started using them as income vehicles in certain client accounts. As these accounts prospered, the firm perceived there to be a steady relationship between large discounts and high subsequent returns. However, they couldn’t find any published research on the relationship between Closed-End Fund discounts and future performance. So, Matisse decided to conduct and publish their own research.

In 2008, Matisse Capital sponsored a study with the Cameron Center for Finance and Securities Analysis (Lundquist College of Business; University of Oregon). Together Bryn and Eric Boughton, CFA (Matisse Capital’s Portfolio Manager and Chief Analyst) pushed the study forward; the first of its kind. Boughton was an applied mathematics major at the University of Houston, where he had the highest GPA in the College of Natural Science and Mathematics. Bryn describes him as a spreadsheet junkie and Bloomberg terminal wizard who was essential to completing this study.

The study’s goal was to analyze Closed-End Fund performance dating back to 1988, all to answer one question: Do large discounts lead consistently to higher total returns?

As they would find, after compiling over 85,000 individual data points from Bloomberg and old newspaper clippings, the answer was a statistically significant yes.

Matisse found that historically for US Closed-End Funds, discounts to NAV have been highly correlated with subsequent total returns. The results were statistically significant across time, and across different Closed-End Fund types. Over the time-period studied (1988-2009), a simple investment strategy based on discounts demonstrated impressive long-term results (20% annualized return; 0.7 beta and 13% annualized alpha to the S&P 500).

“That [University of Oregon] study laid the foundation for just about everything we do today,” Boughton explains. “We have of course refined our processes over time. But our strategy, the way we manage money, and our investment thesis all stem from the research we did with those graduate students.”

As Bryn points out, Nik was actually in the business school at Oregon while they wrapped up the study. Nik graduated from Oregon’s Lundquist College of Business honors program and is a current MBA and MIMFA candidate at Creighton University (while he continues to work full-time at Matisse). “Now he’s transitioning into our institutional marketing role where he’ll attend national conferences and service clients around the country”.

Maybe the Best Investment Strategy You’ve Never Heard Of

Matisse Capital’s Discounted Closed-End Fund Strategy is quite mechanical and quantitative by nature. The Matisse team analyzes all 480+ Closed-End Funds daily through its private, live-updating proprietary database. Matisse lists out every Closed-End Fund from top-to-bottom by its current discount, splits the universe into fifths (or quintiles) based on discount levels, and then focuses only on funds in the most discounted fifth. From there, a proprietary quantitative scoring system and years of professional experience take over to determine actual trading and timing while working within stated investment parameters.

The Matisse investment thesis is that if you buy a Closed-End Fund trading at a large discount relative to its historical average discount, the discount will most likely close, or revert, to a level closer to its average. “We call this mean reversion. We believe discounts fluctuate around a long-term average level, and value can be captured when a discount strays too far from its average,” Bryn explains.

“We aren’t necessarily hitting home runs with our positions,” Boughton notes. “Investing in discounted Closed-End Funds is about hitting singles and doubles. It requires a methodical, tactical, professional approach. We hit for average, not power, and our track record shows this mindset can be successful.”

Studying Closed-End Fund discounts was one thing, but the real-world application of the study and Matisse’s live money track record was compelling. Since the strategy’s inception in January 2006, the audited returns have been +8.8% annualized (as of 3/31/2019).

Building off 6 years of success, Matisse launched a publicly traded mutual fund (MDCEX) in late 2012. It’s available on most trading platforms, with a minimum investment of only $1,000. Matisse does offer separately managed accounts on a negotiated basis for institutions.

Public data shows MDCEX has done well since its launch, receiving a five-star rating for Overall, 3-year, and 5-year periods from Morningstar in the Tactical Allocation category (as of 3/31/2019).

Chart is for visual representation only and does not represent actual returns experienced by an investor.

Chart is for visual representation only and does not represent actual returns experienced by an investor.

Who Could Benefit from Investing

Virtually any investor could benefit. Matisse believes their strategy is well suited for IRAs, retirees, pension funds, foundations, and endowments, given its diversification and ability to produce consistently positive returns and high income.

Some investors use Closed-End Funds as a substitute for bond income, although the expected volatility is higher. Closed-End Funds typically pay 5-6% in annual cash distributions that are fairly steady.

Client suitability is always a consideration before making any recommendation. Bryn explains that Matisse wouldn’t normally put all its clients’ assets into just discounted Closed-End Funds. “Recommendations are made with respect to an investor’s entire portfolio and risk tolerance, among other determinants of overall suitability.”

Risk Management

Closed-End Fund investing, like all investing, involves risk. While Matisse can’t guarantee it meets its investment objectives, it does place a heavy emphasis on diversification to manage risk. “From a diversification standpoint, this is less risky than owning individual stocks or bonds,” says Bryn.

“The reality is: if you have 30 to 40 discounted Closed-End Funds in a portfolio, you actually own thousands of underlying securities,” he says. “And over the long-term, our approach to investing has been successful, to the ultimate benefit of our clients.”

Can I Execute this Strategy Myself?

Closed-End Funds are publicly traded securities and can be purchased by individuals on their own. There are resources out there for individuals like Nuveen’s CEF Connect website, but as Matisse notes, owning discounted Closed-End Funds isn’t the same as executing a discounted Closed-End Fund strategy.

Matisse Capital; 4949 Meadows Rd. Ste. 200, Lake Oswego, OR 97035

Matisse Capital; 4949 Meadows Rd. Ste. 200, Lake Oswego, OR 97035

“In theory, it’s not impossible for someone to try and mimic what we do,” explains Boughton. He says the investor would need a Bloomberg terminal or equivalent data source—which can be a big cost barrier—along with also a technical skill requirement, and a need to understand liquidity constraints in the Closed-End Fund market. Boughton adds: “But mostly, if you can’t sit in front of a computer during trading hours and watch these things move in real-time, making tactical moves, then our strategy isn’t realistically executable for an individual on their own.”

Bloomberg terminal subscriptions cost upwards of $25,000 per year. The average Closed-End Fund trades $1,524,000 (131,000 shares) per day. There are 6.5 hours in a normal trading day (6:30am – 1:00pm PST).

Not to mention, Boughton adds, the public doesn’t have access to Matisse’s “secret sauce”—the quantitative formulas they’ve developed over time that score and rank discounted Closed-End Funds. “Those will always be kept private,” he concludes. “They’re the most important part of the equation.”

The Matisse Discounted Closed-End Fund Strategy is open to new investors. Those interested can call Matisse directly or visit the firm’s website — www.matissecap.com/closed-end-funds — to learn more.

Important Disclosures

Past performance is not a guarantee of future results. Performance cited represents a composite of all Matisse Capital-advised accounts employing its discounted Closed-End Fund strategy, including its publicly traded mutual Fund, net of all commissions, and separate accounts with a presumed 1% management fee.

An investor should consider the investment objectives, risks, and charges and expenses of the Fund carefully before investing. The prospectus contains this and other information about the Fund. A copy of the prospectus is available online at www.ncfunds.com or by calling Shareholder Services at 1-800-773-3863. The prospectus should be read carefully before investing.

The views and opinions expressed are for informational and educational purposes only, and do not constitute any investment advice or recommendation by Matisse Capital.

Matisse Capital is not affiliated or Endorsed by Morningstar, Inc. For more information on Morningstar Ratings, please visit www.morningstar.com/company/morningstar-ratings-faq.

Brand stories are paid content articles that allow Oregon Business advertisers to share news about their organizations and engage with readers on business and public policy issues. The stories are produced in house by the Oregon Business marketing department. For more information, contact associate publisher Courtney Kutzman.