Tax-code changes put nonprofits in a bind.

Last year a new record was surpassed in private giving to charities. Individuals, estates, foundations and corporations were estimated to have contributed a record $390 billion to U.S. nonprofits in 2016, according to a report published in 2017 by Giving USA Foundation, an initiative of the Giving Institute.

Fast-forward to 2018 and the financial outlook for the nonprofit sector couldn’t be cloudier. The Tax Cuts and Jobs Act, an overhaul of the tax code passed in December 2017, is estimated to potentially eliminate up to $17 billion in donations to charities annually, according to the American Enterprise Institute.

The true extent of the financial blow to nonprofits will not be known until the spring of 2019, when data will be available on how much the changes will discourage charitable donations. But nonprofits are already “freaked out” by the dire predictions, says Jim White, executive director of the Nonprofit Association of Oregon.

Nonprofits that will be hardest hit will be organizations that depend solely on private giving to stay afloat. The sector is already under pressure from the tight labor market, which is enticing employees away from nonprofits to better-paying private-sector jobs. Rising health insurance costs and the increase in the minimum wage are also putting the squeeze on the sector.

The change to the tax code that has the most far-reaching impact on nonprofits is the doubling of the standard deduction. For single taxpayers, it goes up to $12,000, and $24,000 for married couples filing jointly.

The fear is that the doubling of the standard deduction will incentivize taxpayers to claim the standard deduction rather than choose to itemize their taxes. This is bad for nonprofits because taxpayers can only claim a deduction for charitable donations if they itemize.

About 28% of money going to nonprofits comes from private donations. Before the tax-law change, about 30% of Americans itemized their taxes. The majority of those people gave money to charities and claimed a tax break. The tax-law change is estimated to lower the percentage of people choosing to itemize to between 5% and 12%.

A possible result of the tax-code changes is that it shifts the incentive to give to charities to wealthier people, who still stand to benefit from itemizing their taxes. This has the effect of concentrating power and influence over the sector in the hands of the rich.

To combat this, the Independent Sector, a Washington, D.C., organization representing large nonprofits, foundations and corporations, supports allowing everyone to claim a deduction on charitable donations whether they itemize their taxes or not. Legislation was introduced this spring to create a “universal charitable deduction.” The aim is to “democratize” the tax incentive, says Ben Kershaw, director of public policy and government relations at the Independent Sector.

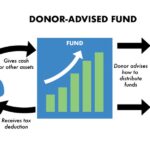

Another way around the tax changes is to increase the use of donor-advised funds. These investment vehicles allow donors to make charitable contributions as frequently as they like. They immediately receive a tax deduction from putting money into the funds, which are invested and grow tax-free. At any time, donors can recommend using money from the accounts to provide grants to charities.

While the tax-code changes portend a fall in charitable contributions, White at the Nonprofit Association of Oregon does not think it spells financial ruin for the sector. For one, Oregonians give at higher rates nationally across every economic group. “We are not attached to that standardization,” he says.

Charitable giving is also correlated to economic trends, such as inflation and cost of living. In 2016, when private charitable donations hit a record, personal consumption and disposable income increased by nearly 4%. As long as the economy continues to strengthen, private giving has a good chance of rebounding.

“We will likely see a drop-off in charitable deductions,” says White. “By 2020 I hope to see it go back up if we don’t see softening in the economy.”

Sorry, No More Bus Passes

A change to the tax code now requires nonprofits to pay tax on transportation benefits provided as an employee benefit. Charities, which typically do not pay income taxes, may for the first time have a tax liability because they provide subsidies to employees for covering the cost of taking public transit and providing free parking.

This tax-code change is likely to hit many nonprofits that take part in Oregon Business magazine’s 100 Best Nonprofits to Work For in Oregon project. Employee-transportation subsidies are a typical benefit of organizations that make it onto the list.

There is a lot of uncertainty over how this section of the new legislation will be enforced. The language of the law is low on details, leaving nonprofits unclear to what extent they will be liable, says Kershaw. The logical conclusion is that cash-strapped nonprofits will cut this employee benefit to avoid the risk of added cost. “Our first concern is to delay implementation until there is more guidance,” Kershaw says.

To subscribe to Oregon Business click here.