Today’s economic uncertainty has not translated into stock market volatility. But we may be witnessing a runaway bull market.

Last week, we came across a headline on the New York Post website alerting readers, “JUST IN: The Runaway Bull Is Dead.” Hopefully this was just an update on an actual bull’s demise and not a prophetic headline for the U.S. equity markets.

But one can argue that it has been a runaway bull scenario. Since the bottom in March 9, 2009, U.S. stocks have been the best performing global asset class — and have also been the least loved. Since March of 2009, investors have pulled close to half-a-trillion dollars out of U.S. equities while stocks have been up over 300%. The chart below highlights the month fund flows into U.S. domestic equity mutual funds and ETFs. For that most part, flows have been out … and the market has gone up.

So why have stocks been soaring when investors have been selling? The answer is: company buybacks.

Bernstein Research estimates that companies announced over $500 billion in share buybacks in the U.S. in 2016, and this is down from $650 billion in 2015. Shares outstanding for large-cap U.S. companies are hitting record lows.

CNBC’s Bob Pasani highlighted this occurrence earlier this month. With company margins at record highs and cash generation remaining healthy, we expect this trend to continue. Finally, should there be a tax repatriation holiday for U.S. companies, bringing back any of the $2.0 trillion of cash held overseas, these buybacks will continue.

Smooth Sailing During Political Turbulence

It’s been more than a month since inauguration of our 45th president, and the momentum in equity markets have continued. Post the election, stocks rallied over 5% into the end of 2016. Our outlook for 2017 was somewhat cautious due to muted earnings growth, uncertainty over new fiscal policies as well as valuation.

What has been a major surprise is the lack of volatility in the markets. Policy and economic uncertainty has not translated into stock market volatility. Some at the Fed expressed concerns about complacency in their January minutes.

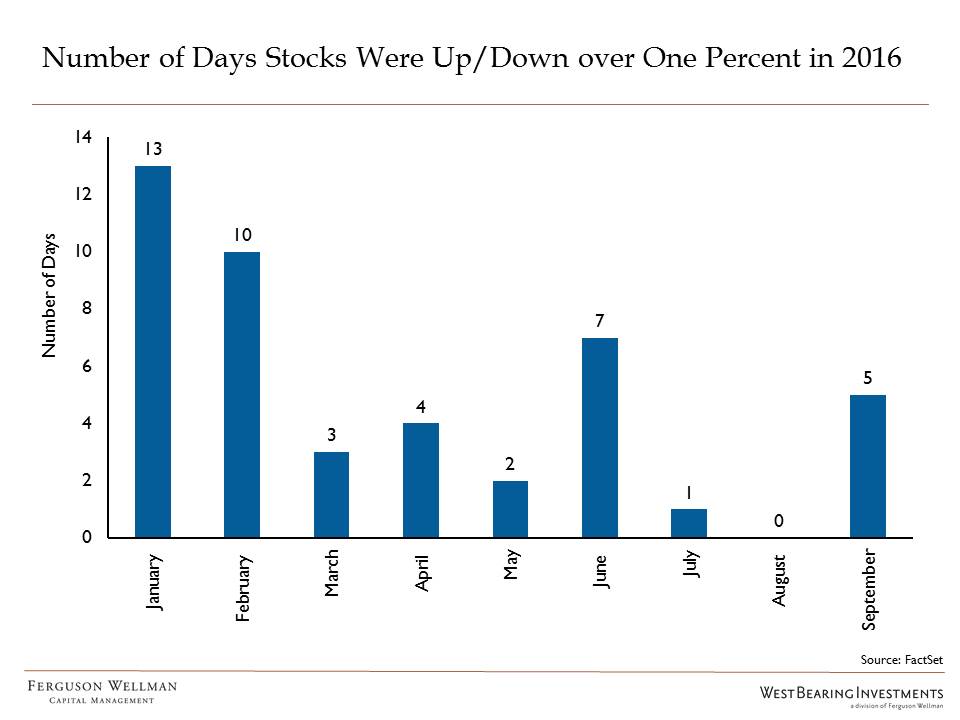

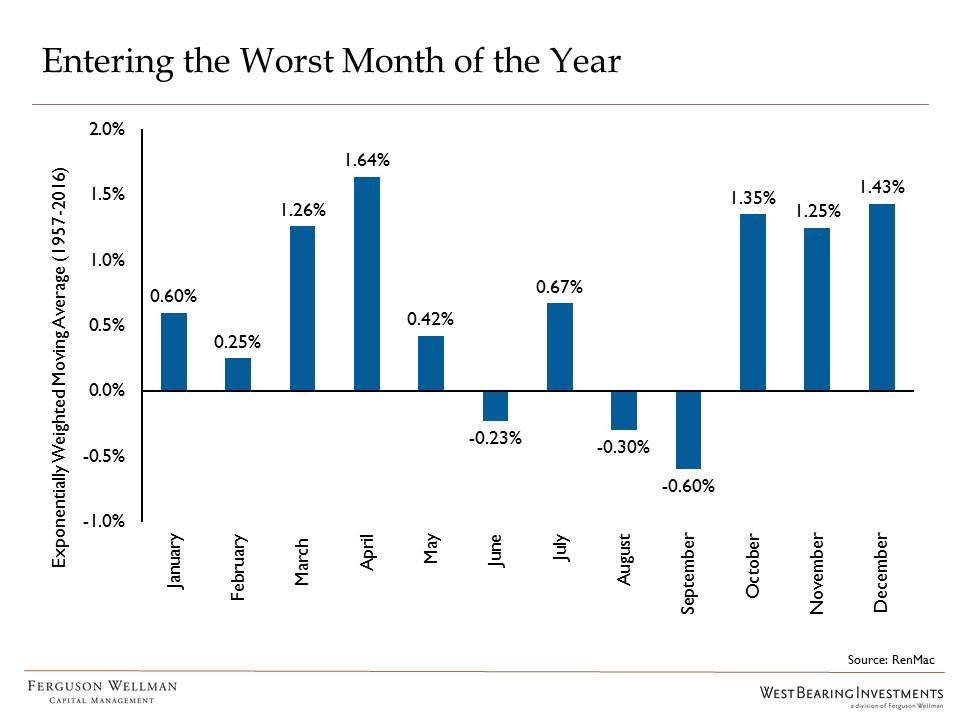

For instance, it has been over 50 days since stocks have moved either up or down more than 1% in one day. It’s been over 90 days since the market has sold off over 1% in a day. Historically, when equity volatility is this low, it has resulted in above-average returns. The chart below shows how often moves up-or-down that were more than 1% have occurred during each year.

When the markets exhibit low daily volatility, it is usually during periods of strength. Note the mid-80s, mid-90s, and mid-00s. Even over the last four years, the S&P 500 is up over 75 percent. This is a 15% annualized return, 5% greater than the long-term average.

We continue to be surprised at how complacent the markets seem to be with uncertain fiscal policy, low global economic growth and valuations that aren’t cheap. Our 2017 outlook was focused on corporate earnings growth being a “show me” story, but investors aren’t waiting for the results, they are buying with the anticipation of good news. The key data point they are looking at is confidence. The chart below highlights the change in confidence from businesses over the last year.

If equities are going to hold their gains, this confidence is going to have to translate into future economic and profit growth.

The Coin Flip: From the global economy to what’s happening here in Oregon

Pockets of Confidence in Oregon

One doesn’t need a research firm to tell Oregonians that confidence is as polarized as politics can be. In just one day, we attended meetings and events in downtown Portland that reflected a wide range of sentiments. Some expressed confidence as high as Mt. Hood’s peak, and others felt as low as Tillamook County flood areas. For purposes of this piece, we took a look at the panoramic view of the optimists.

First, discussion around tax cuts for companies and individuals has been met with the most enthusiasm. A less regulatory environment for companies could translate into higher revenue and increased productivity, but some of our individual clients share the concern, “At what cost?”

As documented in the Oregon Business Morning Roundup, the Boeing Fabrication facility in Gresham announced investment in new systems that will improve production efficiency rather than outsourcing the work to third-party suppliers outside of the U.S.

Although this move won’t create new jobs, it will reduce the likelihood of layoffs and the facility in the future. Intel’s announcement earlier this month at the White House regarding their factory in Arizona was another example of good news for domestic manufacturing that Oregonians hope may trickle back to our state. Our timber towns expressed confidence after the November election that the new administration has the potential to revive their communities through potential changes in trade policy.

Perhaps confidence in our state could best be described through the proverbial glass of water. As Governor Kate Brown said last year in her remarks about state revenue, “We need to quit arguing about whether the glass is half full or half empty ― and instead acknowledge that there just may not be enough water to go around.” Here’s hoping that a better business environment will help quench our thirst.

Jason Norris, CFA, is executive vice president of research at Ferguson Wellman Capital Management. Ferguson Wellman is a guest blogger on the financial markets for Oregon Business.